X-Energy's Immodest IPO

What China's 50-year pebble bed reactor program can teach us about the valuation of the West's most recent publicly traded reactor company.

X-Energy was listed on the Nasdaq under the ticker “XE” on April 24th, raising $1.02 billion with shares surging 30.9% on debut to give the company a valuation of $11.9 billion.

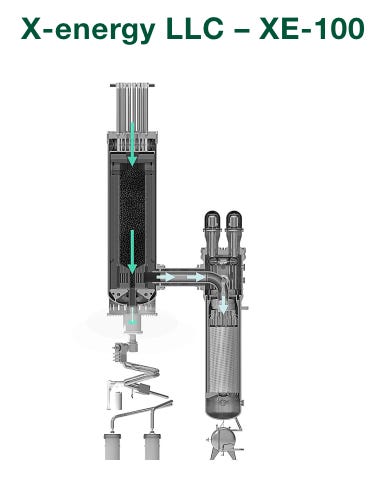

The pitch is Dow Chemical as anchor customer, Amazon as both lead equity investor and holder of power purchase commitments for more than 5 GWe, and Centrica as a UK utility partner, all anchored to an 80 MWe pebble-bed high-temperature gas-cooled reactor.

X-Energy is a 916-person development-stage company promising rapid construction of high reliability reactors fuelled by proprietary TRISO fuel which is roughly 10 times more expensive to fabricate than conventional light water reactor fuel. For a deep dive on that topic, see Decouple’s interview with Michael Seely below.

It has no construction experience, has never operated nuclear reactors, and is yet to produce commercial fuel. Yet it is priced as though the hardest engineering problems in one of nuclear’s least mature reactor classes are already solved.

The current AI-driven moment of nuclear euphoria creates the conditions where this is possible. In the absence of a sustained tempo of nuclear construction in the West, narratives trump empiric reality and reactor concepts that are genuinely interesting science projects get priced as commercial products well before the performance record justifies it.

The embedded assumption in X-Energy’s $11.9 billion valuation is that American startup dynamism can compress what has been for China, the world’s most capable nuclear industrial state, a 50-year institutional journey into a single first-of-a-kind construction project.

In sectors where design, capital, and IP are dominant, that assumption is often correct. China’s pebble-bed program, however, illustrates why even “advanced nuclear” is not one of those industries.

The German Origins and Chinese Technology Transfer of the HTGR

The pebble-bed concept originated with Rudolf Schulten at the Jülich Research Centre in Germany in the 1950s and 1960s. Germany built and operated the AVR and THTR-300 before political and economic pressure killed the HTGR program in the aftermath of Chernobyl.

China then absorbed 30 years of German engineering knowledge through formal technology transfer. This included a design review by Siemens/Interatom of the Chinese prototype HTGR, the HTR-10 in 1994. They have subsequently spent the next 3 decades building on it.

After 5 years of construction the 10MWt prototype reactor achieved criticality in 2000. Construction of the 80MWe commercial demonstration HTR-PM began in 2012, 38 years after basic research started at Tsinghua University.

It would be a mistake to treat those 38 years as a universal law of pebble bed development. For most of that period, especially prior to the 2000s, the program ran at the pace of a modestly funded national laboratory inside a much less capable economy with considerably more pressing industrial priorities than an experimental reactor concept. The China that initiated pebble bed research in the 1970s bore little resemblance to the nuclear industrial state that completed the HTR-PM in the 2010s.

A more concentrated, well-capitalized effort could plausibly move through the design and testing sequence faster, but the historical precedents for that kind of speed, the US Navy reactor programme and the AEC-era national laboratories were state-mobilized at a scale and institutional depth that a private startup has yet to replicate.

The Technology Readiness Level and Capacity Factor problem

The pebble-bed high-temperature gas-cooled reactor is a precise example of the gap between scientific promise of “advanced nuclear” and the commercial maturity of conventional water cooled reactors. Approximately 650 commercial PWRs and BWRs have operated since the 1950s, accumulating 18,000 reactor-years of operational experience.

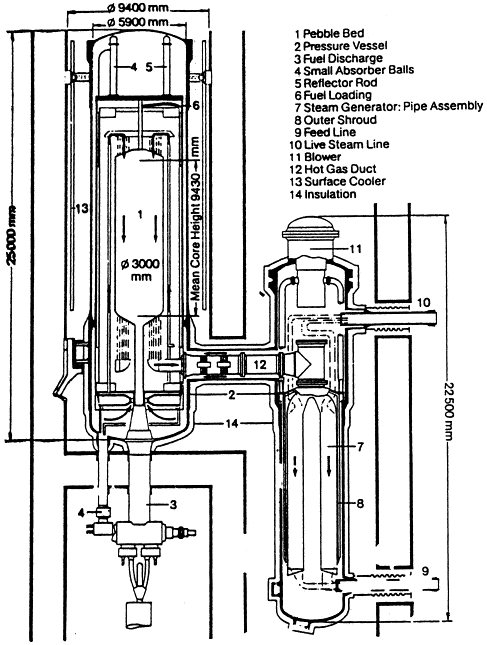

Against that baseline, exactly 5 pebble-bed HTGR cores have ever operated: 2 pilot-scale research reactors, one German and one Chinese and 3 commercial demonstration-scale cores. Those were Germany’s short lived THTR-300 at 120 MWe (1983-1989) and a pair of 80MWe HTR-PM modules at Shidaowan, which reached commercial operation only in 2023.

Commercial demonstration scale pebble-bed HTGRs have thus accumulated only 12 reactor-years of operation to date. X-Energy’s customers are being asked to assume that its reactor technology will automatically share the 90%+ capacity factors that the light water reactor fleet has obtained through 18,000 reactor years of learning and optimization.

Dow and Amazon need high availability and the Xe-100’s central marketing claim is that continuous online refuelling delivers exactly that: no scheduled outages, dispatchable baseload and therefore high capacity factors from day one.

The best way for a lay person to make sense of the pebble-bed online refuelling concept is a giant gum ball machine. The pebble-bed HTGR continuously recirculates hundreds of thousands of fuel spheres through the reactor core, approximately 2000 per day, through a burnup measurement station, and back into the top of the core. This process must function with exceptional reliability as a continuous industrial operation rather than a periodic maintenance event.

As a comparison, the only other commercial reactor type that refuels continuously on a daily basis is the CANDU, which shuffles approximately 15 fuel bundles per day through a well-understood mechanical sequence refined across a fleet of reactors over 50 years. CANDU online refuelling still ranks among the more demanding operational challenges Canadian operators face.

The HTR-PM experience suggests this is harder to sustain than the design predicts. These refuelling difficulties may contribute to the fact that the Chinese plant entered commercial service derated 20% below its design thermal rating and reached only around 20% capacity factor in its first 2 years, advancing to around 50% by 2025.

Critically, China’s engineers entered the HTR-PM’s commercial demonstration phase carrying over 20 years of hard operational data from the HTR-10 research reactor. Problems like fuel handling anomalies, pebble flow irregularity, graphite dust management, helium leaks that manifested at 10 MWt research scale informed the commercial system’s design before a single pebble moved through it.

X-Energy has no equivalent operational foundation. Its fuel handling system has been modelled and tested at sub-scale, and it proposes to move directly from those results to a commercial build at Dow’s Seadrift facility.

The OPEX-CAPEX trade off

The 9 year construction record of the HTR-PM carries a specific warning for the X-Energy investment thesis. The business case for a low-pressure advanced reactor with expensive TRISO fuel, depends on offsetting high operating costs through faster, cheaper construction.

A pressurized water reactor must keep its coolant liquid at around 155 atmospheres, demanding thick-walled pressure vessels and elaborate emergency cooling systems that dominate capital costs and slow construction.

Despite its far lower power density and therefore relatively larger core, a helium-cooled pebble-bed reactor operates at lower pressure with fuel designed to retain fission products passively. The nuclear island should therefore in theory be simpler and faster to build.

Here a construction environment comparison matters as much as the reactor design. China’s construction sector since the 2010s is amongst the most capable nuclear building environments that have ever existed. Chinese builders have been simultaneously erecting conventional PWRs in under 6 years at 2 to 3 times the Western pace, drawing on deep supply chains, and a trained nuclear construction workforce. In that environment, the HTR-PM still took 9 years to build and a further 2 years to commission before entering commercial operation.

X-Energy will build in the contemporary American nuclear construction environment. That environment produced the only 2 AP1000 units completed in America in the 21st century at Vogtle, which came in at roughly 3 times the original budget and 7 years late, under cost-of-service regulation that insulated the project from market consequences throughout.

There is no equivalent rate-base backstop for Dow Chemical. The labour scarcity, the supply chain atrophy, and the absence of a standing nuclear construction workforce are structural features of the American sector, not problems that startup capital resolves. China’s HTR-PM first-of-a-kind timeline, built inside the contemporary world’s strongest nuclear construction infrastructure, is therefore a best case for X-Energy rather than a like-for-like comparison.

The bold claim made by X-Energy CEO Clay Sell in the present tense that “We make it easy to build nuclear power plants” will certainly be put to the test. Extraordinary claims require extraordinary evidence and that evidence has yet to be produced.

The Limits of American Startup Dynamism

X-Energy’s optimism relies on the assumption that American entrepreneurial dynamism will trump Chinese state development of advanced reactor technology.

This dynamism clearly works where iteration cycles are short, failure is recoverable, and the feedback loop between experiment and result is measured in months: shale drilling, rocketry and software are the cardinal examples.

SpaceX can destroy many prototypes on a single launch pad, absorb the data, and fly again within months. However, even an “advanced” nuclear reactor takes years to build with each reactor requiring its own seismically qualified civil works equivalent of a launch pad. In addition, its components must operate without failure for years and breaking things at the commercial reactor stage is not an option.

The iteration cycles, the failure intolerance, and the manufacturing precision of nuclear requirements impose longer timelines and slower iteration. This is what China’s HTGR program illustrates and no amount of venture or retail capital changes that.

But surely a peppy startup can move faster than a state run program in China?

The Western image of China as a cumbersome mass manufacturer of cheap goods rather than a technology leader is desperately out of date.

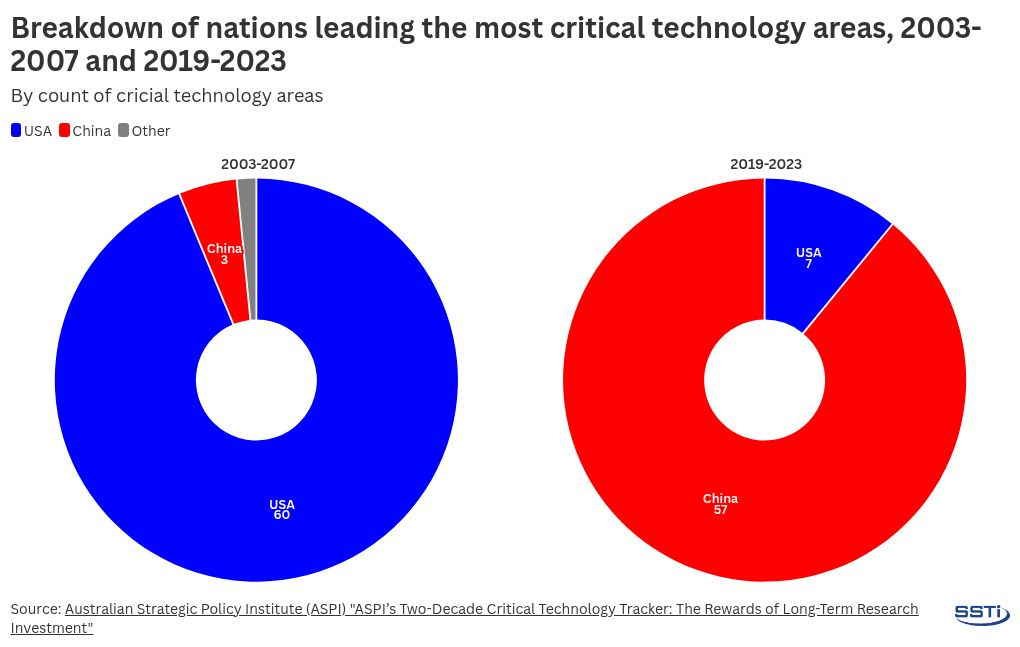

The Australian Strategic Policy Institute’s Critical Technology Tracker found China leading in just 3 of the technologies it tracked during 2003 to 2007. By 2024 that figure was 57 of 64, with nuclear explicitly among them. The country X-Energy is being benchmarked against, implicitly or otherwise, is not the China of 2003.

This is due to aggressive industrial policy and state capacity organized within a hybrid political economy. America’s nuclear reactor technology development dominance with the PWR/BWR similarly leaned heavily on robust state involvement to nurture the technology through its early development.

What China has built in pebble-bed HTGR technology over the last 5 decades is the capacity to cycle continuously from materials research through fabrication to operational deployment and back, accumulating compounding institutional learning at each pass.

X-Energy proposes to move from blueprints to commercial reactors at Dow’s Seadrift plant in under a decade, and according to Amazon’s commitment, envisions 5GW of capacity across the US by 2039.

X-Energy is a genuinely interesting technology company working on a compelling reactor concept. However, the entire history of pebble-bed HTGR development argues against the idea of leap-frogging the pilot and demonstration reactor stage and proceeding directly to a commercial build.

China ran the HTR-10 for over 2 decades before turning on its commercial scale demonstration reactor and is only now upsizing from its 2 module configuration to a fully commercial 6-pack, the HTR-PM 600 in the hopes of improving the small reactor’s challenging economics.

X-Energy has no equivalent to the HTR-10 or the HTR-PM. The comparison that ultimately matters is not how long China's program took in calendar years, but what China brought to its commercial demonstration that X-Energy does not: 2 decades of dedicated research reactor operational data, the world's most capable nuclear construction sector, and cost-of-service regulation backstopping the learning curve.

$11.9 billion is an immodest price for a firm that, by its own timeline, proposes to do something more ambitious than what China attempted, with less preparation and in a more difficult construction environment.

Chris - Like China X-Energy hit the ground running with the help of tech transfer from Germany. They hired a substantial portion of the HTGR technical team when South Africa put that project into a long hiatus.

X-Energy may not have much construction experience, but Dow is the licensee and will be the power plant constructor. X-Energy is the technology supplier.

X-Energy received a $1 B addition to its cash war chest. That’s a powerful development tool.

You’re correct in pointing to the importance of the refueling system. It’s an area worth watching.

So 11 billion is an immodest amount of money to develop a new reactor? I get you are doubtful, doubtful, wary. But what are you writing this for? Investor protection? You believe that 13 years is super fast for a reactor development? Much of the reactor can be tested without turning it on. If allowed to turn on, a reactor can be built and destroyed after a year. Then reconstructed. It is a carefull “stewardship” of resources that prevents this, not something inherently dangerous. With enough resources a space-X approach is possible.