Was Nuclear Ever Cheaper Than Coal?

Understanding the Birth of America’s Nuclear Power Industry

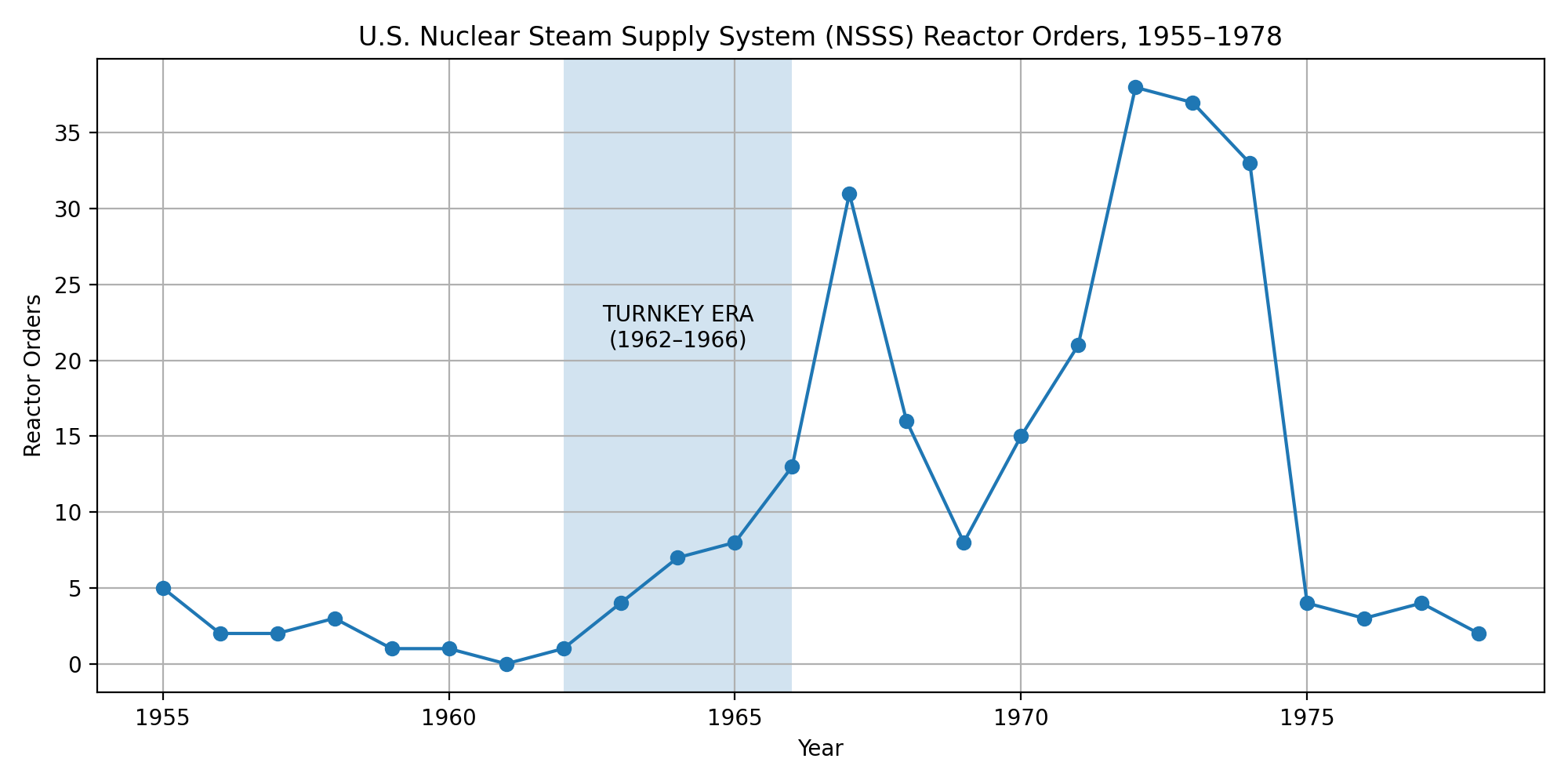

In the early 1960s the U.S. nuclear industry went from stagnation to the fastest sustained growth for any major industry in the country’s history.

Throughout the mid 1950s to early 1960s attempts by the Atomic Energy Commission to kickstart a power reactor industry through fuel subsidies, R&D support and even reactor ownership in the form of the Power Reactor Demonstration Program (PRDP) disappointed.

The economics and performance of these experimental reactors: SMR sized light water reactors and a smattering of what have come to be called “advanced reactors,” were so unconvincing that in 1961 there wasn’t a single reactor order placed by a US utility.

Philip Sporn, the CEO of American Electric Power and among the most respected utility executives in the country, put the consensus plainly in the early 1960s: a nuclear plant would cost 50% to 100% more than a coal plant.

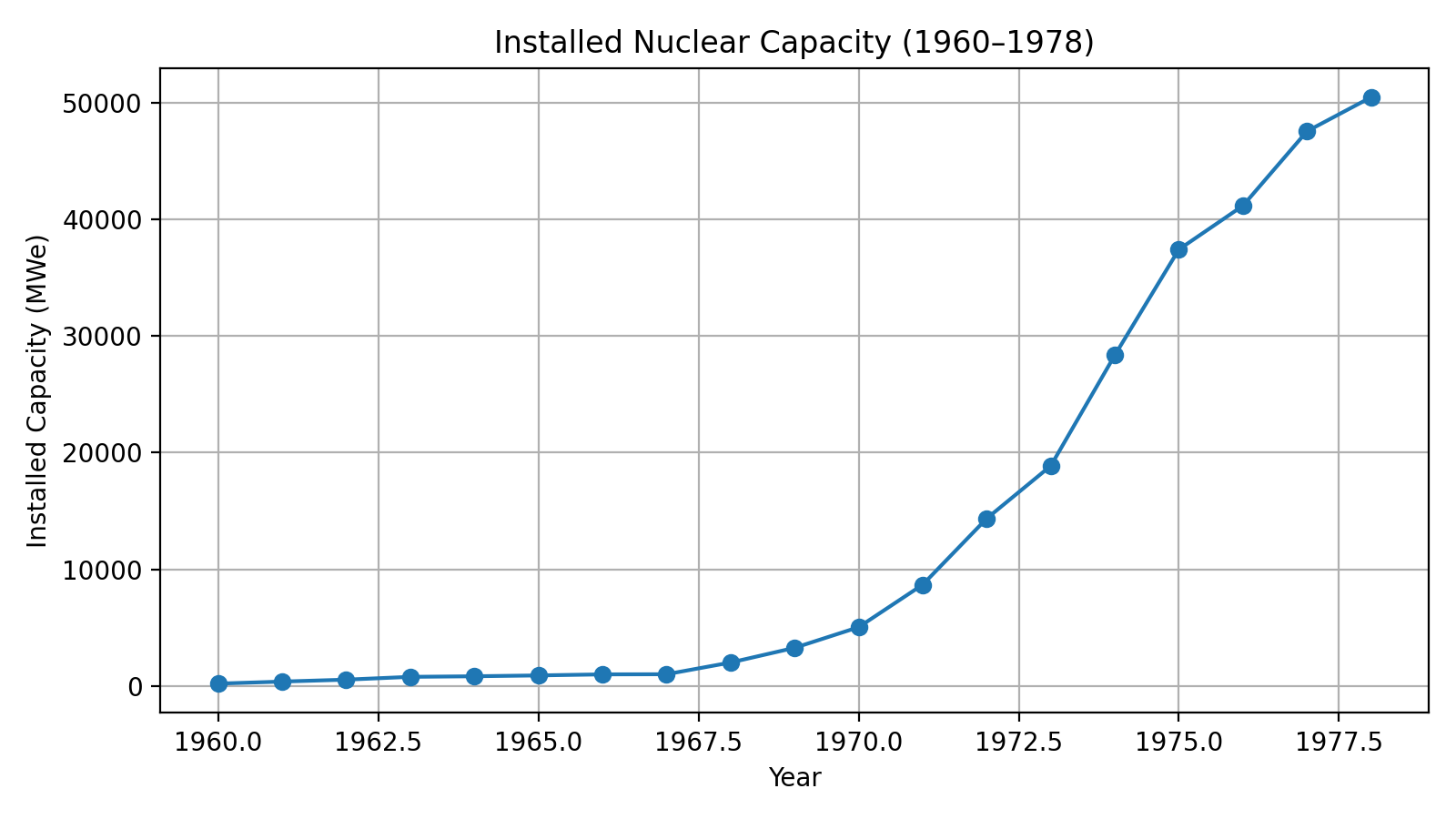

However from 1962-1976 installed nuclear power capacity grew 40% year on year, doubling roughly every two years going from 200MW in 1960 to more than 50GW in 1977.

The Extraordinary Turnaround

Between 1962 and 1966 Westinghouse and General Electric offered 13 turnkey reactors to utility partners at fixed prices competitive with coal. They sold those plants at roughly half of what they cost to build, kept the books closed, and ate losses that in several cases exceeded the entire sale price.

The “nuclear cheaper than coal” golden-age benchmark referenced by advocates that anchors decades of nuclear cost commentary was perhaps the most consequential marketing campaign in the history of American infrastructure.

What is amazing is that when Westinghouse and GE ceased offering these fixed price contracts in 1966 orders exploded. Utilities were convinced that they could build reactors for even less.

This deep dive of the American Nuclear industry’s origin story, inspired by my interview with James Krellenstein on the Decouple Podcast, explains why.

The Context of the Turnkey Era

The two firms that decided to crack open a struggling market were unlike anything in the modern financialized American economy.

General Electric and Westinghouse had electrified the United States. In the 1960s, as the grid continued to double every 10 years, they manufactured almost every component from generation to consumption of electric power: steam turbines, generators, switchgear, transformers as well as washers, dryers, and stoves.

They also financed power plants through their credit arms, ran broadcasting operations, built locomotives and jet engines, and sat at the center of the military-industrial complex. Nuclear was a small fraction of their revenue, and almost all of it was defense work on the rapidly increasing bomber, submarine and nuclear deterrent forces during the missile-gap years.

The commercial logic for offering turnkey fixed price contracts was straightforward. Both companies had deep relationships with every utility in the country. They knew that utilities wanted to diversify away from coal as fuel costs were projected to rise and urban air pollution was becoming a hot button issue.

GE and Westinghouse believed that a single credible demonstration of nuclear power at coal parity could open the floodgates.

Nuclear Power Cheaper than Coal?

In December 1963 they made it so. Sort of.

General Electric signed a contract with Jersey Central Power & Light to deliver Oyster Creek as a turnkey project. Realizing that economies of scale had the greatest chance of improving the disappointing economics of the PRDP era, this BWR was designed to be 650 MW, three times larger than the Dresden 1, the largest reactor then operating. It was a firm fixed price of $132 per kilowatt in 1963 dollars, with GE acting as designer, constructor, and guarantor, handing over a finished plant no matter what it cost to build.

For that site, the price beat coal. Jersey Central said so publicly, and emphasized that it had selected nuclear on economics alone, with no AEC policy considerations attached.

These orders cascaded. GE followed up with six further large boiling water reactors. Westinghouse, unwilling to cede the market, answered with five large pressurized water reactors all on firm fixed prices.

What the buyers did not see was the gap between price and cost. The AEC’s own estimates, assembled later, are stark. Jersey Central paid $90 million for Oyster Creek; GE spent an estimated $170 million building it.

Point Beach sold for about $145 million and cost Westinghouse an estimated $329 million, a loss of $184 million that exceeded the entire purchase price.

Across roughly a dozen turnkey plants, the combined losses came to about $1 billion in 1960s dollars, north of $10 billion today.

The end of an era

By the summer of 1966 the losses had become intolerable, and General Electric and Westinghouse stopped offering fixed price contracts. From the vantage point of 2026 the reaction was puzzling.

Electrical World, the trade publication of record, ran an editorial on July 4 1966 where the editors predicted that returning control to the utilities would deliver lower costs than the vendors’ fixed prices ever could.

The reasoning was that GE and Westinghouse must have been padding their bids with contingency, and a utility with active ongoing experience competently running large projects with a large rate base could self-insure that risk and build even cheaper.

The rate base did more than absorb risk. Under cost-of-service regulation, a utility earned its guaranteed return on capital invested, with little or no margin on fuel and operating expenses, and prudent cost overruns could be passed through to ratepayers.

A nuclear plant, maximally capital-intensive and minimally fuel-dependent, was the most attractive object a regulated utility’s profit-and-loss statement had ever encountered. The incentive structure that would later prove ruinous looked, in 1966, like alignment.

The order book exploded. From 1962 to 1976 almost the entire American fleet, still the largest in the world in 2026, was built or under construction.

For a brief window, some utilities did build genuinely cheap plants. Palisades, Peach Bottom 2 and Browns Ferry had experienced architect-engineers, a hot supply chain and economies of scale which pushed the capital cost of the best-run plants low enough that, once fuel costs were factored in, were competitive with coal not on a capital cost but on a total-cost basis.

The Cost Plume

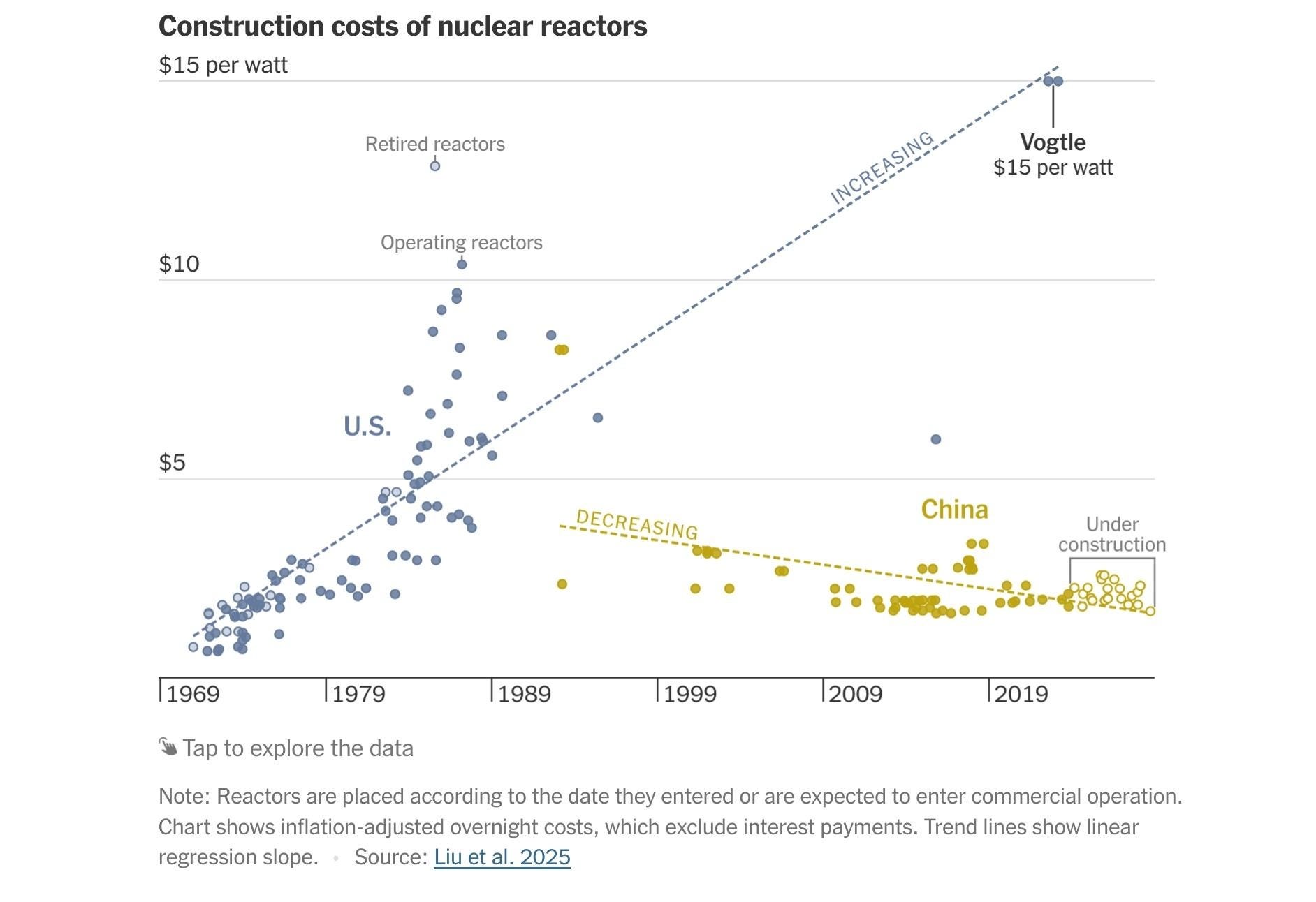

However, between 1966 and 1974, the nominal cost of building a nuclear plant rose roughly five-fold. The first leg of that increase, before 1969, came from rising labor costs, falling construction productivity, and economy-wide inflation that doubled coal plant costs at the same time.

Regulation then compounded cost increases from the early 1970s. The 1971 Calvert Cliffs decision forced full NEPA compliance and environmental review into licensing, and the 1972 Giambusso letter imposed high-energy line break and pipe whip analysis. The plants ordered in the boom absorbed these requirements mid-construction.

Then load growth slowed and stalled. Utilities discovered they had ordered plants they no longer required and the cancellation wave of the late 1970s and early 1980s followed. The cost-plus structure that had made nuclear attractive to utility balance sheets now meant ratepayers were funding abandoned reactor projects.

Lessons for our time

The context of the turn key era shares some similarities with our current moment. In 1962, nuclear faced cheap coal, skeptical utilities, and an empty order book despite recent incentives. In 2026 swap in cheap gas, utilities scarred by Vogtle and Summer, generous tax credits and one gets a sense of deja vu.

In some ways we sit in a better position than 1962. We have refined operating “nth” of a kind designs like the AP1000 which has reversed some of the material bloat imposed by earlier regulations. In addition, nuclear regulation is more stable than in the post-Three Mile Island era. Part 52 reduced one of the major cost drivers of that period: late-stage regulatory ratcheting, where plants could be redesigned while already under construction.

However, after the fallout of Westinghouse’s substantially fixed price contracts for Vogtle and Summer and Areva’s fixed price self-destruction at Olkiluoto 3 the days of western reactor vendors offering these kind of contracts seem to be decisively over.

The industrial behemoths of the 1960s that could purposefully price their turnkey plants below cost and shrug off billion-dollar losses as a customer acquisition expense are gone.

Russia, China and South Korea continue to offer fixed price contracts. The West, however, lacks an entity with the demonstrated skills to reliably deliver projects and the enormous balance sheet capable of offering a guaranteed price.

Who will take the risk to enable a renaissance?

The hyperscalers are sometimes nominated for the role, but their nuclear deals so far are power purchase agreements. These lock in demand at a price and leave the construction overrun risk with the developer. In the United States, awash in shale gas, the hyperscalers have cheaper, faster, and above all lower-risk ways to power a data centre.

For the last decade the 50 to 300 MW small modular reactor paradigm was thought to be the way out of this impasse. The vision borrowed from the combined-cycle gas turbine: a largely factory-fabricated set of modules, shipped and assembled on site quickly, at a price low enough, on the order of a billion dollars, that a utility or even a private buyer could carry it on its own balance sheet.

The trouble is that as SMRs moved from slide decks to firm cost estimates, the obvious reasserted itself. A nuclear reactor is not a gas turbine. The inherent costs of a seismic category-I foundation, radiation shielding, bespoke components, spent fuel handling infrastructure and security rivaled large plants like Vogtle on a per kW basis.

The most recent move is to retreat even further from economies of scale towards 1-10 MW micro reactors. Perhaps this scale could enable a new turnkey era at a smaller quantum of capital, one where a micro reactor vendor could credibly guarantee a price because the downside is survivable. The problem is of course that small scale nuclear has always been expensive nuclear. Those arguing that the future will be different are under an enormous burden of proof.

The first turnkey era was the escape from small reactors. Together Westinghouse and General Electric’s race towards GW scale reactors spawned the largest nuclear fleet in the world. If, as some governments have claimed, we want to triple nuclear energy by 2050 construction risk needs to be managed. In the absence of the industrial champions of the past government looks at this point like it will have to take a dominant role.

Like this post to help Decouple hit economies of scale

Excellent post, really interesting. I'd love to know more on how the French case played out, where as I understand it the State did take direct charge of the country's powerful nuclear build-out. I get that the US has the largest fleet in the world, but France today has almost 1 GW per million people, more than three times the US level. It’s impressive and almost all of it a direct result of the Messmer Plan, back in the 1970s. I hope I get to read about that someday, if you have material on it. Thanks

GE and Westinghouse invented the playbook every technology industry has run since. Sell below cost to create the impression of a viable market. Let the customer build confidence on a price that was never real. Then stop subsidising and hope the demand survives the correction. The nuclear industry discovered what happens next in the 1970s when costs rose five-fold and the order book collapsed. Uber discovered the same thing when the $5 ride became the $25 ride. AI labs are in the middle of discovering it right now.

The parallel to the current moment is almost exact. Brad DeLong wrote yesterday about the end of the "$5 Uber era" for AI, where frontier labs are raising prices because the subsidy no longer makes strategic sense. The structural question is the same one GE faced in 1966: did the subsidised period create enough genuine demand that customers will pay the real price, or did it create demand for a price that never existed? Nuclear's answer was that utilities wanted cheap nuclear, not nuclear. When cheap disappeared, so did most of the enthusiasm. Whether AI's answer is different depends on whether the productivity is real enough to survive the bill.