Europe Forgot the Lesson the 1970s Oil Shocks Once Taught

The continent answered with reactors, pipeline diplomacy, and offshore drilling, then spent three decades neglecting and dismantling everything it had built.

The Puzzle the Market Is Posing

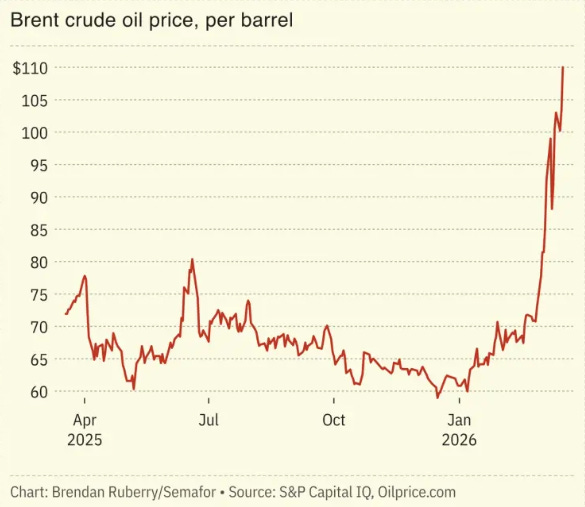

Doomberg is back on Decouple. As one of the sharpest numerically-grounded voices writing about energy markets, he opened our recent conversation with a puzzle: given everything that has happened, the numbers simply should not look like this.

Venezuela’s president was arrested and extradited to New York, the United States imposed an embargo on Cuba, and a hot war with Iran has left the Strait of Hormuz closed and tankers sunk. Iranian missiles destroyed two liquefied natural gas (LNG) trains at Qatar’s Ras Laffan industrial complex, taking roughly 17 percent of Qatari production capacity offline for an estimated five years, while Ukraine continued its campaign against Russian oil tankers and refineries.

Had you presented that full scenario to any energy analyst six months ago and asked them to price oil, almost nobody would have said $98 West Texas Intermediate (WTI) and $110 Brent. Most would have taken the over on $150 without a second thought.

The relative calm in price action requires explanation. Oil’s share of global primary energy has fallen from around 50 percent at the time of the 1973 Arab oil embargo to roughly 35 percent today, meaning a given volume disruption transmits less shock into the broader economy than it once did.

The actual supply disruption running through the Strait of Hormuz is currently around eight to ten million barrels per day rather than the theoretical maximum of twenty, and China alone holds 1.5 billion barrels of strategic reserve, enough to absorb five million barrels per day of that shortfall for 300 days if deployed at scale.

None of this means the crisis is trivial. The pain is real and unevenly distributed. The question it poses, especially for Europe, is whether the shock is finally severe enough to force a reckoning with thirty years of decisions that left the continent structurally exposed in ways that were at least partially avoidable.

What the 1970s Actually Built in Europe

The European response to the OPEC embargo was an impressive mobilization that moved decisively and pragmatically taking advantage of the unique conditions available throughout the bloc.

France

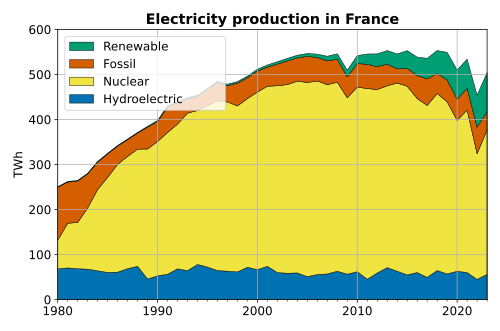

France moved decisively launching the The Messmer Plan in direct response to the oil shock. It remains the fastest large-scale nuclear buildout in history. France had little domestic oil, but it had everything else the program required: a large corps of state-trained engineers produced by the Grandes Écoles, heavy industrial capacity rebuilt under the postwar dirigiste economic model, and a nationalized utility in Électricité de France (EDF) already accustomed to executing at the direction of the state rather than waiting on market incentives.

Its political class drew the logical conclusion: electrify aggressively around a domestic nuclear base, using a standardized reactor designs that a purpose-built supply chain could replicate at pace. Space heating, water heating, rail and significant portions of industrial process heat were shifted onto the grid as the fleet came online, deliberately substituting domestic electrons for imported hydrocarbons across as much of the economy as the technology of the era allowed.

The result over roughly twenty years was 54 operating reactors, an electricity system generating around 75 percent of its output from nuclear, net electricity exports to neighbours who had made different choices, and as an unintentional side effect a per-capita carbon footprint in the power sector that remains among the lowest in the developed world.

Britain Norway and the North Sea

Britain and Norway answered through a different channel with the same underlying instinct. The North Sea had yielded promising geological discoveries before the embargo, but the post-shock period transformed offshore petroleum into a central national project on both sides of the median line.

The technical obstacles were formidable: deepwater fields in rough northern seas, novel platform engineering, supply chain development for equipment categories that had barely existed before.

Both governments pressed through, operating under a governing assumption that sounds almost exotic in Brussels today, namely that a country should develop strategically important resources under its own waters when those resources can materially improve national resilience.

Within roughly a decade Britain had moved from significant oil importer to net exporter. Combined British and Norwegian output contributed materially to the global oil supply glut that emerged through the 1980s. The glut that always follows a supply shock once investment finally responds to price signals was this time in part European.

German Gas Diplomacy

West Germany’s answer came through diplomacy and welded steel. The first Soviet gas began flowing west through the Brotherhood pipeline in 1968, predating Ostpolitik’s formal articulation but embodying its central intuition: that a Russia earning deutschmarks from gas exports had a material interest in stable relations, and that pipelines, unlike armies, are hard to redeploy.

The 1973 embargo deepened that conviction. If imported Middle Eastern oil was vulnerable to political interruption, the answer was to secure more pipeline gas from a supplier with whom West Germany had a structured commercial relationship and a shared interest in its continuation.

The Urengoy-Pomary-Uzhgorod pipeline, completed in 1984 and running from the vast Urengoy gas field in western Siberia to the West German border, was a direct product of that post-shock logic, and it was built over fierce American objection.

The Reagan administration attempted to block European firms from supplying equipment and technology for its construction, arguing that the pipeline would create dangerous dependency. Bonn, Paris, and London essentially told Washington to mind its own business, and the pipeline was completed anyway.

What the gas bought Germany was an industrial cost structure that its European competitors could not match. German chemical producers, steel mills, glassmakers, and ceramics manufacturers built their economics around feedstock and energy costs that were simply unavailable to producers in Britain, France, or the United States.

BASF’s Ludwigshafen complex, the largest integrated chemical site in the world, was in part a monument to cheap Russian gas. Germany became the economic engine of the European Union partly on the strength of that bargain, running large industrial surpluses while its neighbors ran deficits, with cheap energy as one of the structural advantages that made German manufacturing so difficult to compete against.

The results of this collective mobilization were visible by the mid-1990s in a set of numbers worth holding in mind. Europe consumed around 32 EJ of hydrocarbons annually and produced around 15 EJ domestically. Roughly 8 EJ of Russian oil and pipeline gas, operating under long-term contracts with a generally reliable delivery history, functioned as quasi-domestic supply despite transiting through the iron curtain. Effective external import dependence was around 30 percent of consumption.

The French nuclear fleet anchored cheap, firm electricity across much of the continent. North Sea output was near its peak. Groningen, the vast Dutch gas field, underpinned Northwest European supply. Europe had a healthy energetic basis. A continent that had been genuinely vulnerable to a Middle Eastern supply cartel in 1973 had, through two decades of serious state-directed and private sector investment, rebuilt the physical foundations of its own security.

The Pyramid Inverted

That position was dismantled through choices made by a political class that had become unmoored from the physical foundations of its own prosperity.

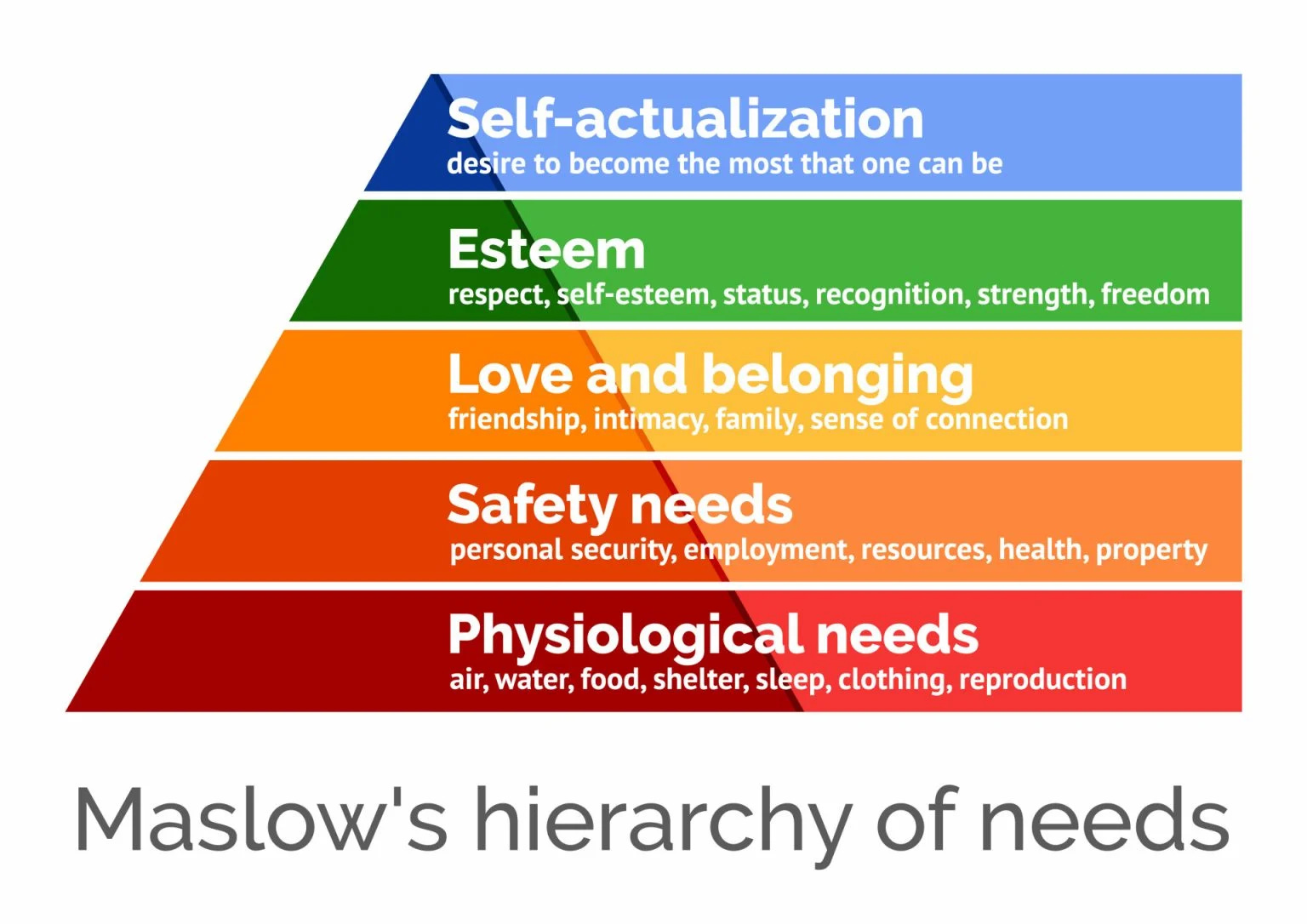

Maslow’s hierarchy was designed as a model of individual motivation, but it maps onto collective political behaviour with uncomfortable precision. A society that has secured abundant energy, industrial production, and physical safety creates the conditions in which political attention can migrate upward into questions of identity, moral positioning, and self-actualization.

The pathology arrives when those governing from the upper floors lose the ability to perceive the importance of the foundations beneath them, and begin making decisions that erode that base in the service of ideological commitments the foundations had made affordable.

By the mid-1990s, Europe had secured its ground floor thoroughly enough that its political class could afford to stop thinking about it. The first Conference of the Parties (COP) climate meeting opened in Berlin in 1995, the same year that marked Europe’s high-water point of energy self-sufficiency. That coincidence is not the whole explanation for what followed, but it is too precise to ignore.

The Decadence of Nuclear Phaseouts

No decision illustrates this dynamic more clearly than the closure of operating nuclear plants. The reactors that came online between the mid-1970s and late 1980s were not marginal facilities at the end of their useful lives. They were industrial cathedrals: vast, complex, irreplaceable concentrations of engineered knowledge representing decades of accumulated operating experience, trained workforces, regulatory culture, and supply chain depth, with low fuel costs, zero carbon emissions, and capacity factors that no other thermal generator could match.

They were shut down because opposition to nuclear power had become a marker of political identity in societies wealthy and secure enough to prioritize symbolic concerns over material ones. The antinuclear movement was a signal of ecological conscience and distrust of technocratic state power that resonated precisely because the lights had stayed on for so long that nobody could imagine them going out.

Germany shut its last three reactors in April 2023, in the middle of an acute energy crisis triggered by the loss of Russian gas, having spent the preceding decade replacing firm nuclear output with a combination of intermittent wind, coal, and imported gas.

The decision was not revisited when the crisis arrived, because doing so would have required the governing coalition to admit that the Green politics it had elevated to the centre of its identity had materially harmed the people it governed. Political identity proved stickier than physical reality, even once the electricity bills surged.

The scale of what was lost cannot be recovered quickly, and that is the point that cuts deepest against any optimism about Europe’s near-term capacity to respond. France still has a nuclear fleet, but it is the aging inheritance of a state that no longer exists in the form that built it.

The engineering workforce that commissioned those 54 reactors has largely retired. The specialized welding trades, the project management systems, the regulatory culture oriented around construction rather than obstruction, all of it was allowed to thin during the decades when new nuclear construction seemed unnecessary and the people demanding it were dismissed as relics of an earlier, less enlightened politics.

When France finally attempted to demonstrate that it could still build, the result was Flamanville 3: a single EPR reactor whose construction began in 2007, encountered cascading quality control failures and design changes, and achieved grid connection only in late 2024 after costs escalated to roughly 13 billion euros against an original estimate of 3.3 billion, a measure of how much institutional knowledge had been lost, and how expensive it is to rediscover what your predecessors once knew how to do.

Europe’s Hydrocarbon Dysmorphia

Today the continent consumes roughly 38 EJ against only 6 EJ produced domestically, with Russian supply now largely severed and Russian LNG under a 2027 phase-out deadline. This represents an extraordinary inversion of insecure hydrocarbon import dependency form 30% in 1995 to 80% in 2026.

The gap between what Europe consumes and what it can produce has widened from something manageable to something genuinely precarious.

The political economy behind this is not simple ignorance. It reflects the triumph of a specific set of assumptions that dominated European governance from roughly the mid-1990s onward. Neoliberalism and Ricardian comparative advantage, applied as governing doctrine held that offshoring industry and supply chains to wherever production was cheapest was rational efficiency rather than strategic vulnerability.

If someone else could supply energy more cheaply than Europe could produce it domestically, the logic ran, then importing was the optimal outcome, and if that someone else also absorbed the climate sin of extraction, so much the better. Europe could signal ecological virtue by de-industrializing while guzzling hydrocarbons produced out of sight and out of mind, congratulating itself on declining domestic emissions that had not so much been eliminated as outsourced.

The post-Cold War liberal international order would constrain the behaviour of exporters through norms, contracts, and multilateral institutions. The physical substrate, the reactors and rigs and pipelines, could be allowed to thin because the market would supply what was needed, and the moral ledger would look clean in the process.

Europe’s oil and gas consumption peaked at roughly 45 EJ around 2005 and has declined to around 38 EJ today, a reduction of around 15%. The European Environment Agency attributes this to a combination of efficiency improvements, warmer winters, higher post-2022 energy prices, renewables deployment, and structural shifts toward less energy-intensive industries, which is a diplomatic formulation for a process that deserves a blunter name: de-industrialisation.

Steel mills, chemical plants, ceramics manufacturers, and glassmakers that once anchored regional economies across the Ruhr, the Po Valley, and the Midlands have contracted or closed, taking their energy demand with them. The continent did not so much reduce its energy consumption as export the industries that consumed it, along with the employment, the tax base, the engineering knowledge, and the supply chain depth they represented.

Each factory that relocated to cheaper jurisdictions removed another supporting beam from the base of Maslow’s pyramid, trading the material foundations of working-class prosperity for lower headline energy consumption figures that Brussels could present as evidence of a successful transition. It was, in the most literal sense, progress measured by what had been lost.

What this framework systematically failed to account for was the difference between efficiency in a stable trading environment and resilience under supply stress. A just-in-time supply chain optimized for cost is the opposite of what you want when the supply is interrupted.

A grid optimized for cheap intermittent renewables is not the same system as one built around firm dispatchable capacity. The assumptions encoded in comparative advantage theory describe a world of frictionless markets and cooperative suppliers, which is occasionally the world that exists and is frequently not.

What Europe Could Still Do, and Why It Has Not Done It

Doomberg made compelling counter-arguments to my EU doomerism. He pointed out that California has roughly as much oil and gas geology as Texas. It produces a fraction of what Texas does because the legal, fiscal, and regulatory environment makes development effectively impossible.

The same circular logic operates in Europe. If exploration is prohibited, companies do not invest to assess and prove reserves. When reserves remain unproven, policymakers point to the low reserve figures as evidence that the resource is not there. The prohibition creates the condition it claims to be responding to.

Groningen, the Netherlands’ giant gas field, could be restarted. The decision to close it was driven by induced seismicity causing structural damage to buildings in Groningen province, a genuine local problem that nonetheless removed a strategically important asset from the European supply picture at precisely the wrong historical moment.

The Norwegian portion of the North Sea is still producing more than three times as much oil as the British side, and while Norway holds a larger share of the basin's reserves, the gap in output reflects policy as much as geology: Norway offers tax incentives for new development and drilled 33 exploration wells in 2025 while the UK spudded none.

Shale-bearing geology exists in Poland, northern England, France, and Germany. A 78 percent marginal tax rate on exploration and production in Britain, combined with a legal prohibition on hydraulic fracturing, does not describe a country that has concluded its geology is inadequate but rather a country that has politically foreclosed on its options.

The honest assessment is that Europe has real options it has chosen not to exercise, and that the human capital and industrial ecosystem required to exercise them quickly has been allowed to thin. A European shale revolution is perhaps not implausible on geological grounds, but it faces a 20-year American head start in drilling technology, a near-complete absence of the service industry infrastructure that makes rapid field development possible, and a regulatory and social environment that has been actively hostile to hydraulic fracturing.

Groningen could be restarted but not without political cost and not without the engineering assessment of what sustainable production levels might look like after years of inactivity.

New nuclear construction could be authorized but the supply chains and workforce needed to execute it at the pace the 1970s demonstrated are not reconstituted by political commitment alone.

What remains to be seen is whether Europe will experience the current crisis as severe enough to unlock the political will to change the framework. The fiscal terms, the regulatory culture, the legal prohibitions, the institutional preferences that have governed European energy policy for three decades are after all choices rather than facts of nature.

The question the crisis poses is whether the pain has finally reached the threshold at which those choices get revisited, or whether the current political class will manage this disruption as they did the 2022 energy crisis, through emergency imports and demand destruction with a return to the same framework when the immediate pressure eases.

China’s Different Theory of the State

The contrast that makes European failure most legible is not another European country that made better choices. It is China, whose energy policy over the same period reflects a fundamentally different answer to the question of what a state is for.

China’s 2024 primary energy figures from the Statistical Review of World Energy are worth reading slowly. Coal supplied 58 percent of primary energy, almost entirely from domestic mines. Nuclear, hydro, and renewables together contributed roughly 12 percent. Oil and gas accounted for the remaining 30 percent, of which about a quarter of the oil and 57 percent of the gas came from domestic production.

The effective Chinese import dependence on total primary energy is around 15 percent. Europe’s equivalent exposure is 80 percent on hydrocarbons alone, against a backdrop of reduced firm electricity generation following nuclear closures.

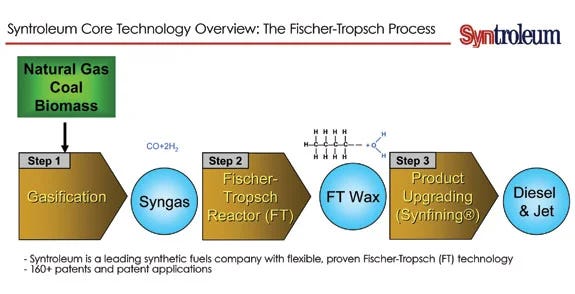

Beyond the headline numbers, China accumulated roughly an additional million barrels per day of crude oil throughout 2025 and stored it in strategic reserves. It built coal stockpiles. It invested in coal-to-chemicals facilities that convert coal through gasification into synthesis gas, the carbon monoxide and hydrogen mixture from which Fischer-Tropsch catalysis can produce diesel, aviation fuel, ammonia, and essentially any hydrocarbon compound a modern economy requires.

Germany developed Fischer-Tropsch synthesis in the 1930s and 1940s under blockade conditions to fuel the Luftwaffe when oil imports were cut off. South Africa built a large coal-to-liquids industry during the apartheid sanctions era. No country builds capital-intensive, carbon-intensive, economically irrational coal-to-liquids capacity for fun.

Countries build it when they are explicitly planning for fuel denial or war. China’s coal-to-chemicals program makes national security sense and no other kind of sense, which is a direct statement of how Beijing’s planners assess their strategic environment.

China also moved to dominate the processing stages of commodity supply chains where it could not dominate the upstream resource. It produces roughly five million barrels of crude oil per day domestically and imports around eleven million, but it has built refining capacity of nearly nineteen million barrels per day, a nameplate figure that dwarfs its own consumption and positions it as a swing supplier of refined products to the rest of the world.

When China banned refined fuel exports within days of the conflict escalating, Australia found itself in difficulty almost immediately. Australia had allowed most of its domestic refining capacity to close over the preceding decade on the assumption that cheaper Asian-processed products would always be available, above all Chinese jet fuel, which had come to supply roughly a third of the country’s aviation needs.

The vulnerability ran from Australian dependence on Chinese refined products through Chinese dependence on Middle Eastern crude to Middle Eastern supply now disrupted: a chain of three links, each individually visible, none apparently prompting precautionary action.

The pattern is consistent across rare earth processing, battery manufacturing, solar panel production, and refining: identify the processing stage where dominance can be created rather than relying on geological endowment and use that position as a buffer against upstream interruption.

This is preparation for a world where the Strait of Malacca can be contested, the first island chain can be used as a coercive instrument and the assumptions of the liberal international trading order do not hold under pressure. Europe read the post-Cold War decades as evidence that those calculations had become obsolete. China saw them as an interval of relative quiet before patterns that have governed great power competition for centuries reasserted themselves.

Can Europe Rebuild its Energy Foundations?

Doomberg holds as axiom that supply shocks reliably produce the investment responses that eventually create gluts. The 1973 embargo produced the North Sea, the Messmer Plan, the IEA strategic reserve system, and eventually a global oil surplus by the mid-1980s. The 2008 financial crisis and $147 nominal crude produced the capital desperation that drove the U.S. shale revolution to commercial viability. Something analogous will emerge from the current crisis, though its precise shape is not yet clear and the degree to which Europe contributes is questionable.

The optimistic reading is that the current disruption finally forces decisions that the 2022 crisis did not. The options are real: Groningen could be restarted, North Sea acreage could attract development capital under different fiscal terms, and Europe’s commitment to new nuclear construction, if sustained, will in theory produce operating capacity, though the timeline will be measured in decades rather than years.

The political conditions that produced the Energiewende, that justified closing operating nuclear plants in the middle of an energy crisis, were themselves the product of Europe’s masterful response to the 1970s energy shock.

The question now is whether Europe can turn its focus to the material basis of its well-being and restore its energy foundation.

Fantastic. We will see by next winter what the choice Europeans make will be. My guess is that it will take much more pain before rationality, forced by steps down on Maslow’s ladder, push European countries to make the tough choices they have put off. It is just as likely, probably more likely, that the EU comes apart.

Europe has been suffering from a nasty case of luxury beliefs. Governments rapidly need to understand that they are responsible for a few basic requirements to their citizens/ subjects and energy security is one of those.