The Nuclear Fallout of an AI Meltdown

The nuclear sector’s political rehabilitation over the last five years has been one of the more remarkable reversals in modern energy policy. Climate politics brought the left onside, created a rare bipartisan consensus resulting in tax credits and generous incentives under the Biden administration. Russia’s invasion of Ukraine hardened the energy security case and tapped the brakes on European nuclear phaseouts. Then came roaring AI datacentre demand narratives, which infused the sector with the promise of lucrative power purchase agreements and cold hard venture capital transforming nuclear energy into a speculative asset class.

Oklo, which merged with Sam Altman’s SPAC in 2024 at an $850 million valuation, reached a peak market cap above $30 billion in 2025, largely on AI electricity demand expectations. Microsoft is reportedly paying $115/MWh for the revived Three Mile Island’s output under a 20-year contract, roughly double historic PJM wholesale prices.

The nuclear sector should not bite the hand that feeds it, but it should examine its palm lines very carefully, because there are now serious reasons to believe the AI demand narrative rests on questionable economics and over investment in an LLM-centric approach. While the technology has seduced many and has genuinely important use cases, limitations are emerging that may be intrinsic to LLM architecture itself.

The exploration of the evidence indicating an AI bubble is inspired by the accompanying podcast interview with returning guest David Helmer founder and managing partner at NTTW consulting. Stick around for the conclusion where I share my thoughts on which nuclear players get hit hardest.

Symptoms of an AI Bubble

Frontier labs have been reporting annualized run-rate revenues of $25 to $30 billion. These murky figures are calculated by multiplying a single strong month by twelve, often at a moment when a product launch like Claude Code can distort numbers well beyond their representative averages. Even accepting those numbers, they sit against enormous training and inference costs, in the case of OpenAI, roughly $600 billion through 2030. All of these compute costs pale in comparison to the supporting infrastructure investments in chips, server racks, datacentres, power and cooling which McKinsey projects to reach 6.7 trillion in capital expenditure by 2030.

Three years after 100 million users were collectively wowed by the Eliza effect of a purposefully designed human-like GPT3 chatbot, subsidized use is still the rule. It is the same playbook Silicon Valley used to underwrite cheap Uber rides and discounted DoorDash deliveries to upend traditional incumbents and establish market share. Sam Altman acknowledged in January 2025 that OpenAI was losing money on every $200/month ChatGPT Pro subscriber, with heavy users consuming an estimated $5,000 in compute: a 25-to-1 subsidy ratio.

The glitch with the LLM subsidy strategy is that the per-user cost of frontier AI is an eye wateringly expensive data centre, not a low wage driver’s time and unlike taxi rides and takeout food no one has yet demonstrated that the users who showed up for the subsidized LLM product will follow it to true market price.

In the absence of organic revenue what is propping up these investments is in part what technology analyst Azeem Azhar has called a “financial ouroboros:” the same capital cycling through chipmakers, cloud providers, and frontier labs in a closed loop. A single point of demand failure could now propagate through every balance sheet in the chain simultaneously.

The agentic era was supposed to be where the economics finally worked. However, early deployments are raising questions. Uber deployed Claude Code to roughly 5,000 engineers in December 2025 and exhausted its entire 2026 AI token budget by April, with heavy users burning $500 to $2,000 per month. The COO subsequently admitted the company could not draw a clear line between that spending and improvements in consumer products. Global research and advisory firm Gartner projects that enterprise AI bills will rise through 2030 even as per-token costs fall, because agentic workflows consume between 5 and 30 times more tokens per task than standard chatbot interactions. While still early in the technology’s deployment, a July 2025 MIT study of 300 enterprise AI deployments found that 95% delivered no measurable P&L impact.

Willingness to pay significantly more depends on products which are truly economically transformative. The obvious prize is white-collar labour displacement, a 5 to 10 trillion dollar opportunity. However, the predictions of Microsofts AI CEO, Mustafa Suleyman, in February of this year that most tasks that involve “sitting down at a computer” will be fully automated by AI within the next year or 18 months is looking increasingly outlandish. While there has been a junior white-collar slowdown brewing over the last few years it is largely explained by the extraordinary numbers of people hired by tech companies between 2020 and 2022 on the assumption that pandemic-era growth was permanent. ‘We are restructuring toward an AI-first workforce’ lands better with investors than ‘we hired 40,000 people we did not need during a zero interest rate frenzy,’ and CFOs have not been shy about exploiting the ambiguity.

LLM architecture a dead end?

Despite our hardwired tendency to anthropomorphize coherent language production stretching all the way back to Joseph Weizenbaum’s primitive ELIZA chatbot, Large language models are at their core next-token predictors: highly sophisticated auto-complete. They generate confident outputs that sound correct by pattern-matching against a vast training corpus but outside of domains like coding and mathematics, where outputs can be tested against an external ground truth, the model has no equivalent check on whether a fluent sentence happens to be a true one.

The resulting hallucinations and reliability problems appear not to be a temporary deficiency that more training data or compute will resolve. Initially scaling impressed researchers with emergent properties like multi-step reasoning and in-context learning such that it was informally codified into a scaling law. However the phenomenon seems to have plateaued with focus shifting to post training optimization. OpenAI cofounder Ilya Sutstever has stated that the age of scaling is ending and we’re back in the age of research. Yann LeCun, who spent 12 years as Meta’s chief AI scientist, departed in late 2025 to found AMI Labs on the explicit thesis that hallucinations are intrinsic to the LLM architecture rather than fixable with more data. “LLMs are too limiting,” LeCun stated. “Scaling them up will not allow us to reach AGI.”

These comments should raise skepticism about all in bets on a massive infrastructure and compute spend to support a technology that may not be able to meet expectations sufficiently to earn the revenues necessary to pay back the extraordinary investments.

The Fallout of an AI meltdown

If the AI bubble deflates, the nuclear sector absorbs collateral damage in proportion to how closely a given project was tethered to that capital.

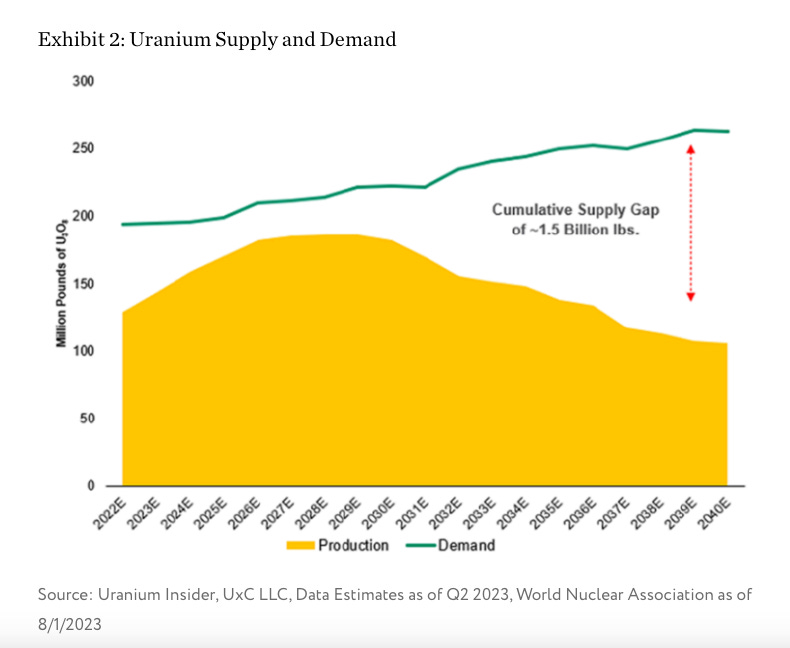

Uranium fundamentals remain intact regardless of what happens to Nvidia’s valuation. Commercial inventories are thin. The secondary supply sources that suppressed prices for 30 years are gone. A projected gap of more than 1 billion pounds between utility requirements and currently visible supply over the next 20 years looms over slow but steady demand growth from China, India, and Russia’s export program.

A speculative correction will likely push uranium spot prices down, as financial buyers exit and risk-off sentiment dominates. This however could worsen the structural deficit heading into the 2030s as lower prices could delay investment in new mines that must come online quickly to narrow the supply gap.

The advanced reactor companies that tech giants chose as partners occupy a more precarious position. The logic behind those choices reflected what might charitably be called disruption bias: a narrative driven tendency to reach for what are being portrayed as “advanced” reactors held back by overzealous regulation while an inferior conventional reactor fleet failed to make good on the promise of electricity too cheap to meter.

Each tech giant has chosen its own distinct advanced reactor darling, a pot pouri of technologies that have frustrated previous efforts to commercialize them. Meta chose the sodium fast reactor vendor Oklo, Google chose a TRISO fueled molten salt cooled reactor concept being developed by Kairos and Amazon chose the recently IPO’d pebble bed high temperature gas reactor start-up X-Energy.

All of these companies are in the protoype stages. None have a licensed, operating commercial reactor design. Each one is asking its “Magnificent Seven” patron to co-finance the creation of industrial supply chains, regulatory precedents, and fuel fabrication infrastructure that does not yet exist at commercial scale.

Uprates are the most defensible position in a correction scenario. The construction risk is lower, the grid interconnection is already built, and the incremental capacity comes online on a timeline measured in years rather than decades. See my interview below with James Krellenstein and Robb Steward of Alva Energy Inc. for the bulls case for this kind of “boring nuclear” additions.

If demand projections are revised significantly downward as the AI data centre buildout slows, stranded baseload generation becomes a genuine utility-sector fear and the business case for large new builds weakens materially. Demand certainty is the foundation beneath every capital-intensive, long-duration, high-risk energy project, and that AI driven demand certainty looked considerably more solid in 2023-2025 than it does today.

The projects most likely to survive a bursting AI bubble are the ones that were least dependent on AI demand projections or venture-capital patience: refurbishments, uprates, and the least technologically speculative new build reactors, those that already have a licensed design, an operational history and a utility customer with growing demand not solely dependent on AI datacentres.

Without a genuinely transformative AI product that can command prices reflecting actual compute costs, the capital cycling through chipmakers, hyperscalers, and frontier labs has no exit other than a correction. Nuclear investors who have anchored their business cases to data centre demand projections made at the peak of that cycle should be doing the math on what their projects look like if those projections are halved.

Like this post. Tokens of appreciation are free and help us to bring you more great content.

Very North American view.

In Continental Europe (especially the Low Countries and CEE) the fundamentals for grid demand are very strong (including continued electrification policies) and current wholesale electricity prices easily support new build nuclear even at LCOEs like the FOAK plant at DNNP without needing RAB. Plus energy sovereignty, already on the agenda and even more so since Hormuz. No AI boom needed.

What’s held Europe back is their suicidal anti-nuclear policies of the last forty years, now quickly disappearing, as well as the bureaucracy, permitting, and NIMBYism that also holds back Canada. That’s quickly disappearing too as industry begins to genuinely pack up and leave due to prices and politicians start to panic.

AI bubble bursting will indeed hurt US deployments. (Especially agree on the Oklo and Aalo types tied most closely to Big Tech.) There is however a world beyond the US, and I think it’s waking up from its 30-year Pax Americana slumber.

This is excellent = Thank You. Aside from what looks like crazy risk to be linking unlicensed new nuke designs with projected (wishful) AI generating real profit, did you catch discussion on whether or not safe, 10,000 year storage of fissile waste has really been worked out? I was in the tunneling industry 27 years, knew two guys who went to Hanford & Yuca Mountain jobs. I ran into both on two different tunnels a span of years later. Both said the engineering / mega term storage wasn’t proven & the projects shut down.