The Gas Turbine: The final revelation in the pantheon of prime movers.

Why it arrived last and why the West still dominates

Rockets, in the form of gunpowder charges rammed into bamboo, predate the Magna Carta. Water wheels powered medieval grain mills. Steam piston engines drove the industrial revolution and Parson’s 1894 steam turbine continues to deliver most of the world’s electricity generation. In the late 19th century Otto’s and Diesel’s internal combustion engines began to reorganize transportation, agriculture, warfare and bulk shipping of commodities.

The gas turbine emerged only in the 1930s. It is the most recent and the last prime mover. It has subsequently become the undisputed champion of global aviation and increasingly a dominant source of dispatchable electricity on grids around the world. Demand for gas turbines is now surging as AI data centres require rapid additions of baseload power.

John Barber patented a recognizable gas turbine cycle in 1791, describing a compressor, a combustion chamber, and a turbine wheel in sequence. John Brayton worked out the thermodynamic cycle that still bears his name in 1872. By the time Frank Whittle ran his first jet engine prototype in 1937, engineers had been sketching versions of the same concept for 65 years.

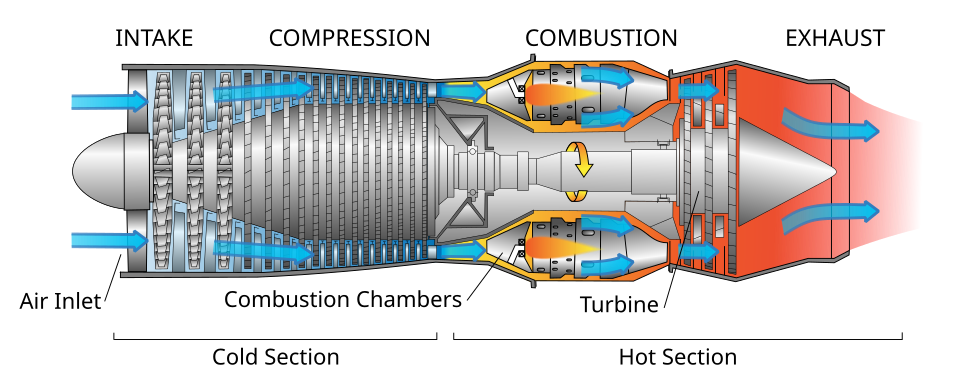

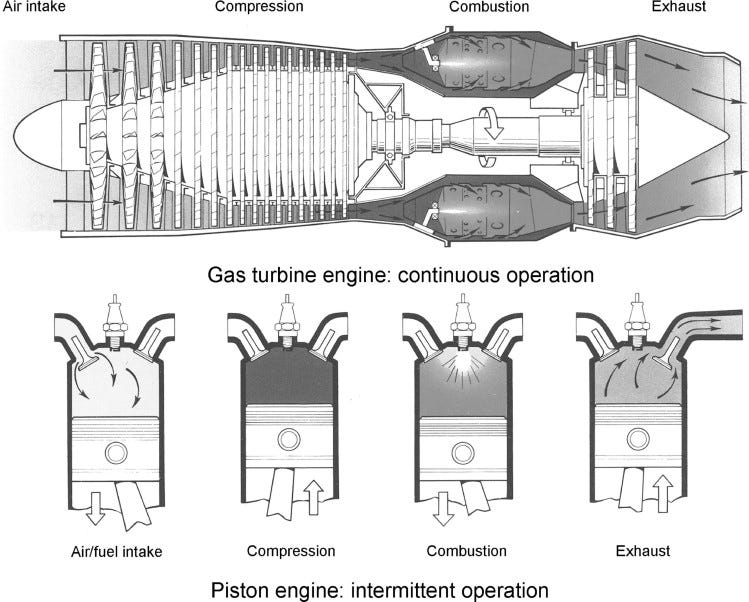

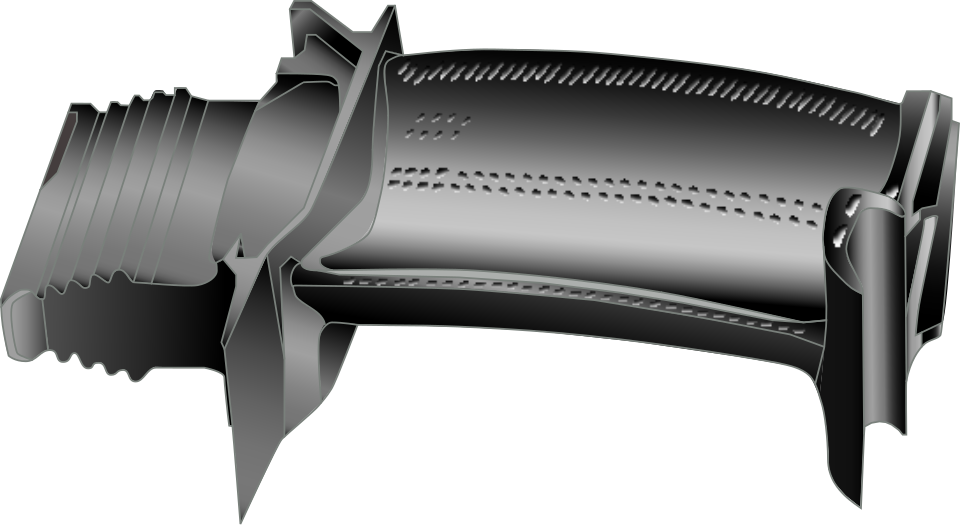

A gas turbine is, at its core, a device that compresses air, adds fuel and combusts it to produce extremely hot gas to spin a turbine. As engineers push the thermodynamic limits through hotter temperatures the engineering reality is that the hot gasses leaving a modern combustor are well beyond the melting point of the alloys from which the turbine blades are made.

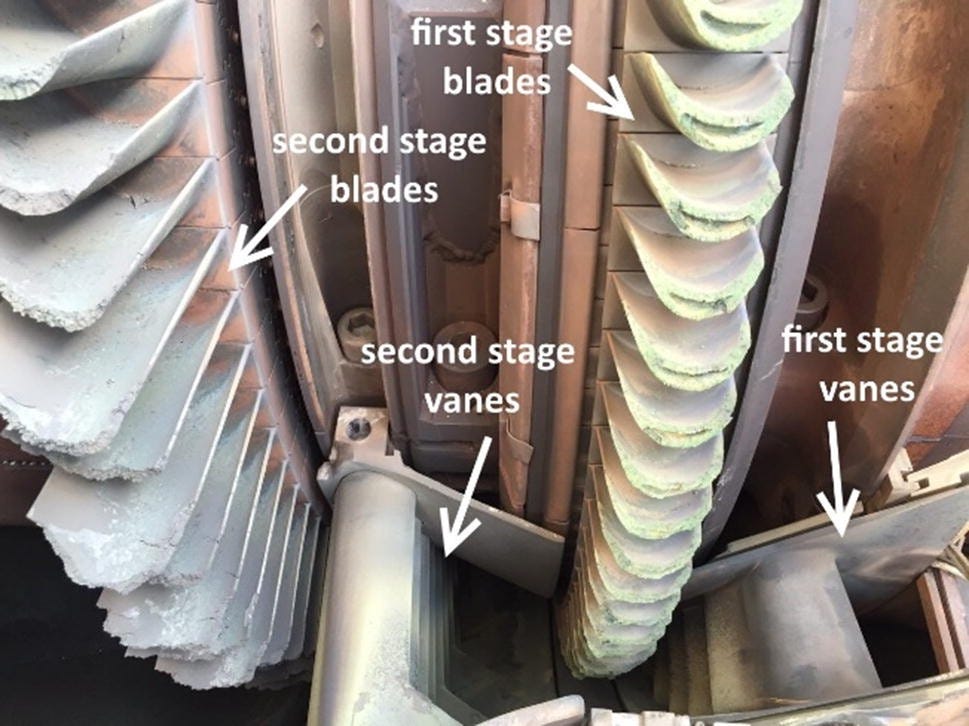

The compressor in a large commercial engine reaches pressure ratios above 40:1, requiring blade geometries machined to tolerances measured in microns across components spinning at thousands of revolutions per minute. In aviation applications the containment structure must be light enough to fly and strong enough to survive a blade release without sending a fragment through a fuselage.

The extreme safety and reliability requirements in aviation and power generation impose a slower pace in innovation cycles reminiscent of the nuclear industry. In the end the gas turbine’s limits are defined by the cumulative materials and manufacturing knowledge required to operate at the edge of its thermodynamics. These factors determine who can build it, and why it is one of the few technologies that the West still decisively dominates, for now.

The following essay is based on a conversation on the Decouple Podcast with Dr. David Helmer, a veteran of GE Global Research and the American Society of Mechanical Engineers (ASME) K-14 gas turbine heat transfer committee.

The impetus for the development of the gas turbine

What finally shifted the gas turbine from blueprints to a functioning engine was the pressures of a World War in which aviation had become increasingly central. Through the 1930s, piston engines remained the only practical option for powered flight, and their limitations were becoming a military liability.

Piston engines struggle at higher altitudes, where thin air starves combustion and power drops sharply. They are mechanically complex, with hundreds of reciprocating and rotating parts subject to vibration, wear, and failure. Their power-to-weight ratio, while adequate for the propeller aircraft of the era, left little room for the performance gains that military planners were demanding: greater speed, higher altitude, longer range. Frank Whittle in Britain and Hans von Ohain both recognized that the piston engine had reached a ceiling that the Brayton cycle could break through.

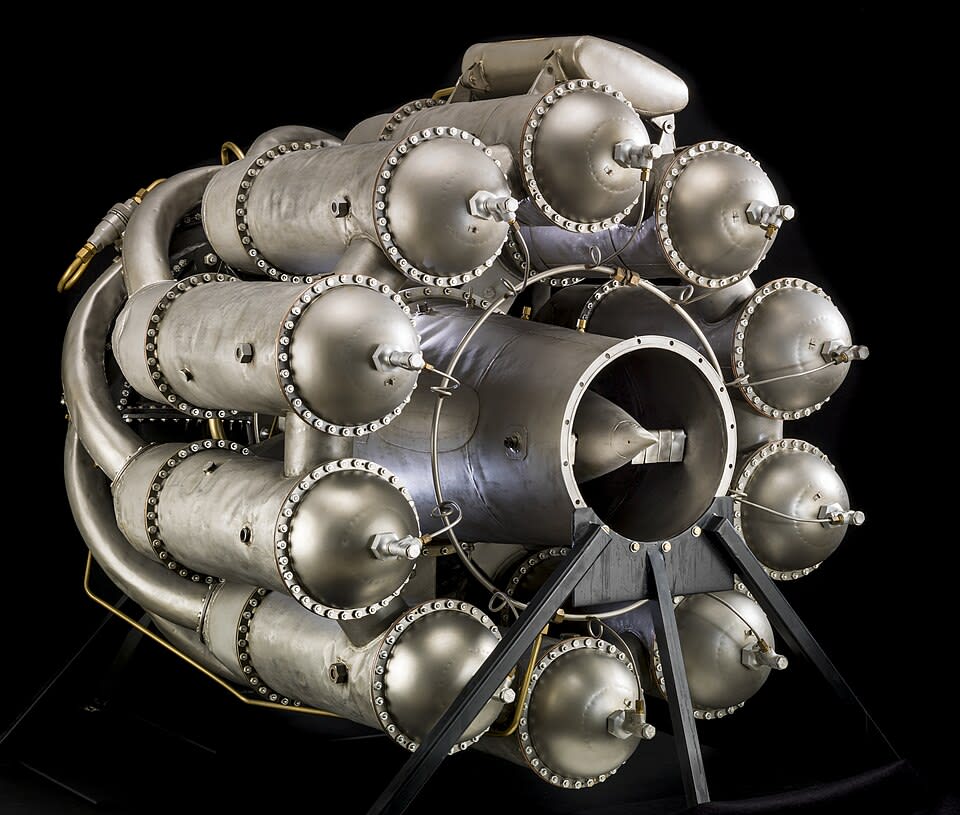

The early engines were extraordinary in concept and crude in execution. Whittle’s W.1, which powered the Gloster E.28/39 on its first flight in May 1941, produced 860 pounds of thrust and had a service life measured in dozens of hours before its primitive nickel alloy components failed. The materials problem, which would come to define the entire subsequent history of the technology, had to wait.

What the war years established, beyond the basic feasibility of jet propulsion, was the industrial and institutional foundation that would separate the countries that could build serious gas turbines from those that could not. Britain transferred its early jet technology to the United States during the war which seeded GE and Pratt & Whitney’s programs and gave American manufacturers a running start they have still not yet relinquished. Germany’s early expertise withered due to the destruction of industrial infrastructure, postwar restrictions on German military aviation and the migration of engineers into allied programs after the war. They only recovered in 1960-70’s but this time in the heavy frame gas turbine power generation market.

The know-how embedded in these technology transfers was only partly captured in drawings and specifications. Much of it lived in the hands and judgment of engineers and machinists as tacit knowledge.

The material science miracles of the modern gas turbine

The central engineering challenge of the gas turbine is that it operates in conditions that should destroy it. Hot gas leaving a modern combustor reaches around 1,500 degrees Celsius. The nickel superalloys used in turbine blades begin to lose structural integrity at temperatures several hundred degrees below that. Engineers have spent decades developing systems to keep them alive: internal cooling channels machined into the single crystal turbine blade itself, thermal barrier coatings and the superalloys doped with rhenium that extend the temperature range the metal can tolerate before creep and fatigue set in.

The design philosophy imposed by the extreme conditions within the engine has no real parallel in other high-stakes engineering domains. A turbine blade in service is always degrading or in the parlance of the industry “experiencing distress.” It cannot however fail catastrophically. The first turbine stage can be “mostly missing,” burned back by inadequate cooling or a material defect, and the engine will often still fly for many more flight cycles until measured degradation crosses a defined tipping point. The system is designed to tolerate continuous partial failure of its most stressed components because pushing to the edge of material limits is the only way to achieve the power density, fuel efficiency and longevity that modern aviation, and power generation demand.

This approach, coupled with the incredibly high safety stakes involved in commercial aviation, requires extensive evaluation. That risk management focus imposes a conservative innovation cycle well familiar to those knowledgeable about nuclear power. A modification to a commercial jet engine requires bench testing of the component in isolation, then stand testing under representative operating conditions which sometimes includes the rigors of the famous chicken gun and blade out scenario. Next is flight and endurance testing for hours accumulation, and finally aircraft recertification if the change affects airframe performance.

The gap between the GE90 and its successor the GE9X is roughly 25 years, a near irreducible time required to validate changes in a system where GE applies 6 sigma quality standards across its engine programs or fewer than 3.4 defects per million.

For reference SpaceX which has moved at lightning speeds in its rocket development is able to accept an engine failure rate of roughly 1% across its launch program.

Gas Turbines go Terrestrial

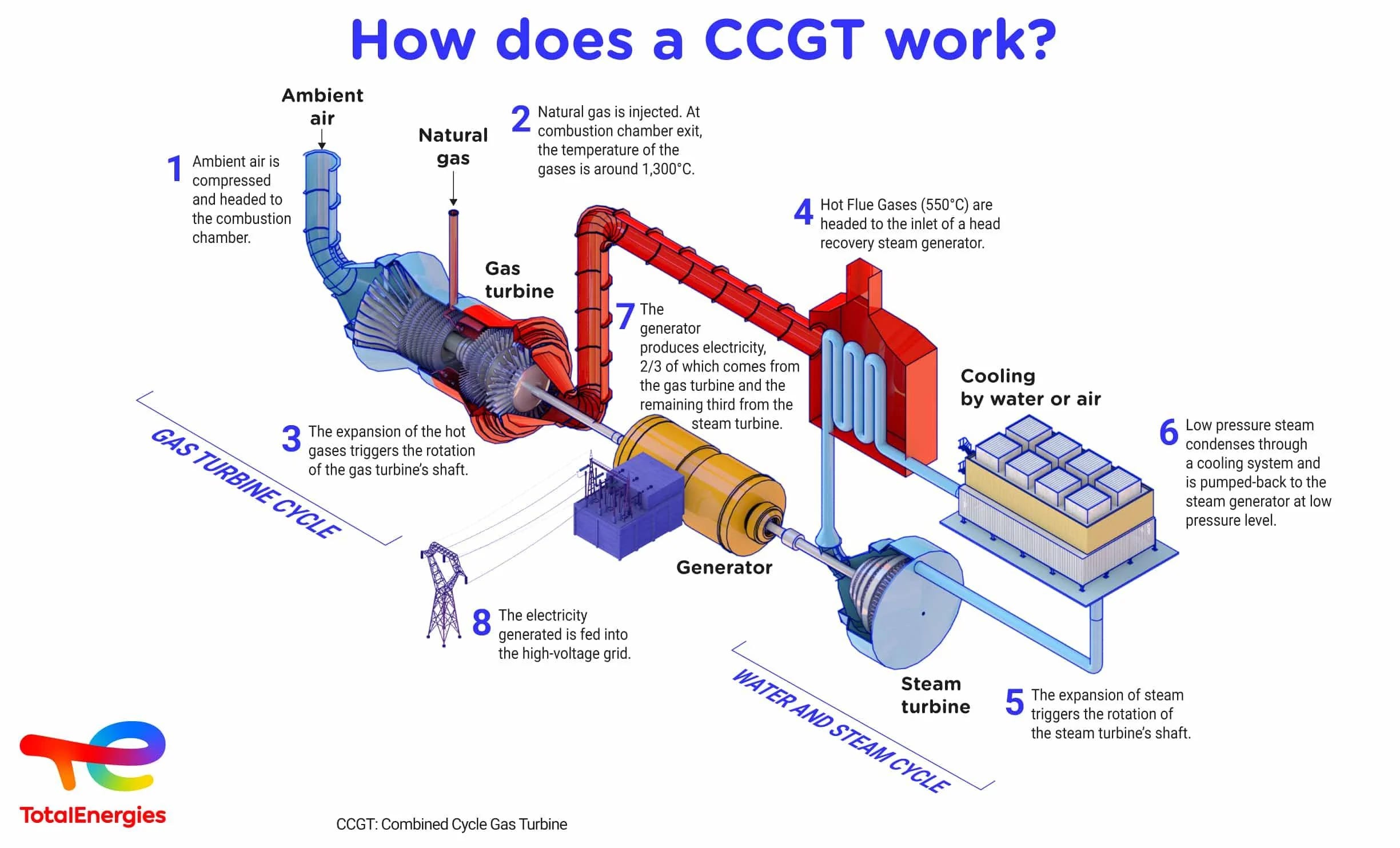

When a gas turbine leaves the aircraft and gets bolted to the ground, some of the engineering constraints relax. Weight stops mattering and bird ingestion becomes a smaller problem but precision engineering around performance and reliability still matters. Unlike a jet with relatively short duty cycles, a utility turbine may be asked to run continuously for weeks, while every small loss in efficiency compounds into fuel cost and every excess maintenance outage becomes lost revenue.

The most interesting design option that became available to terrestrial gas turbines, however, was the potential to use their extremely high quality waste heat which averages 550 degrees Celsius. A gas turbine in simple cycle operation, running alone without any additional heat recovery, converts fuel to electricity at thermal efficiency in the low to mid 40s percent. Unlike an aircraft, where that heat is simply dumped into the ambient air, on the ground it can be routed into a heat recovery steam generator, which uses it to boil water and drive a steam turbine in a second, separate power generation cycle.

Early combined cycle plants existed decades before, but the concept only became commercially transformative in the 1980s and 1990s as improved materials, higher turbine inlet temperatures, blade cooling, digital controls, and increasingly sophisticated combustion management pushed gas turbine performance high enough to make the economics compelling. Combined cycle plants could now exceed 50 percent thermal efficiency and eventually move past 60 percent, allowing natural gas to compete directly with coal for sustained baseload electricity generation rather than merely serving as an expensive peaking fuel.

At the same time, deregulated electricity markets were expanding across North America and Europe, rewarding technologies with lower upfront capital costs, shorter construction schedules, and operational flexibility. Combined cycle gas turbines fit that environment unusually well.

They were efficient enough to run continuously, could ramp up and shut down far more easily than coal or nuclear, and avoided fuel costs entirely when offline, an important advantage in volatile merchant power markets. Environmental pressure on coal was also rising due to concerns over sulfur dioxide, particulates, mercury, and eventually CO2 emissions, areas in which natural gas is a demonstrably cleaner alternative to coal.

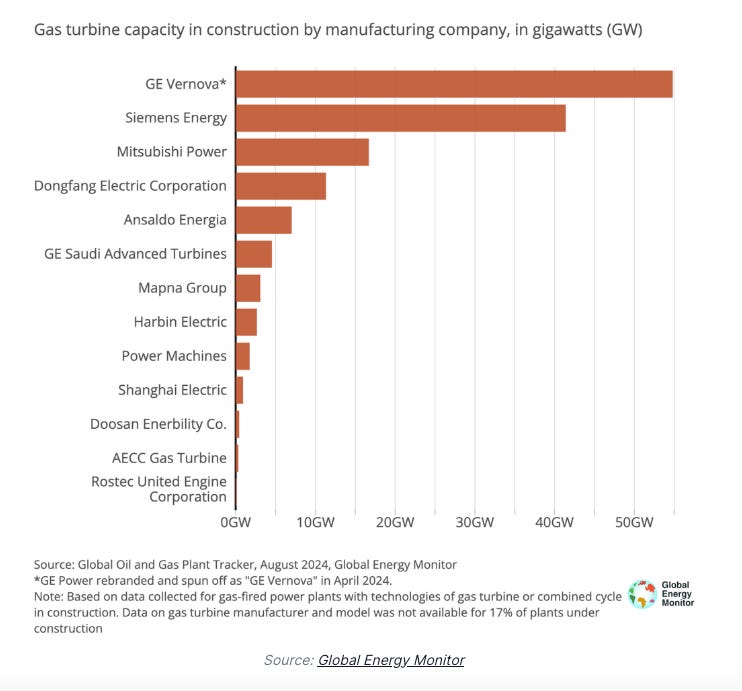

GE, Siemens Energy, and Mitsubishi Heavy Industries spent the late 1990s and early 2000s expanding manufacturing capacity aggressively around the assumption that the world was moving toward a gas dominated electricity system built on combined cycle gas turbines. Annual heavy duty gas turbine orders reportedly reached 120 to 140 gigawatts globally in the early 2000s.

Then a perfect storm hit. The 2008 financial crisis crushed electricity demand growth across much of the OECD, wind and solar rapidly absorbed incremental generation growth and the merchant power boom had already saturated the American market with relatively new gas plants. Global heavy-duty turbine orders fell to roughly 30 to 40 gigawatts annually by the mid-2010s, a collapse of more than two-thirds from peak.

The consequences were severe: massive layoffs, factory underutilization, write-downs, collapsing margins, and an investor confidence collapse that fed the broader GE crisis of the late 2010s. Under Larry Culp, GE eventually broke itself into 3 separate companies: GE HealthCare, GE Vernova, and GE Aerospace.

Today GE Vernova, Siemens Energy, and Mitsubishi face another major positive demand shock driven by AI data centers and electrification, with delivery queues stretching toward the early 2030s. This time none of them are expanding recklessly recognizing the possibility of an AI bubble, a strategic stance somewhat akin to the newfound capital discipline in the U.S. shale patch that evolved after its most recent price collapse.

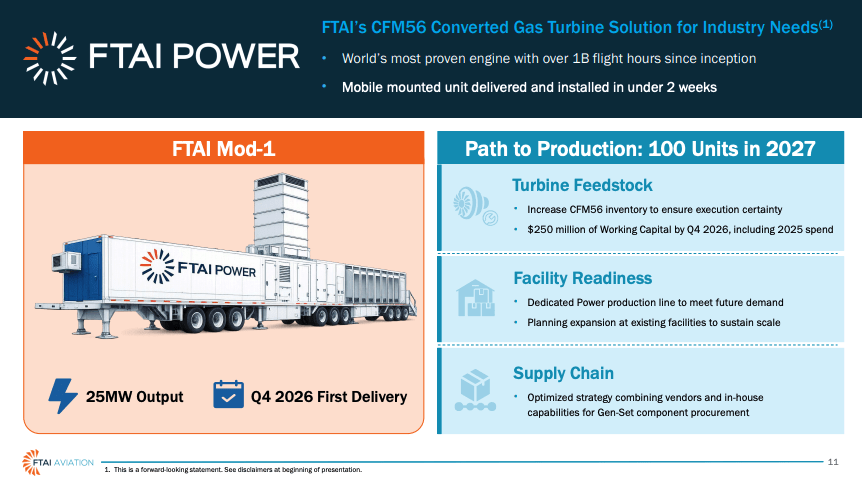

The gap is being filled by companies like FTAI power which is currently taking CFM56 engines off retired commercial aircraft, converting them for ground-based power generation, and selling that capacity to data centers that cannot wait for purpose-built equipment.

Why the West is Still Dominant in Gas Turbines

Commercial jet engine manufacturing is one of the most concentrated industries on earth. GE Aerospace, Rolls-Royce, Pratt & Whitney and France’s Safran produce essentially all of the turbofan engines powering large commercial aircraft.

Fighter jet engines operate under a different set of constraints: shorter service lives, no six sigma safety requirement, and performance prioritized over durability. Both Russia and China have developed credible military engines on that basis, but the jump from a capable fighter engine to a certified commercial turbofan is a different engineering problem entirely.

So why has that dominance proven so durable despite decades of well-resourced attempts to break it? The answer has several mutually reinforcing layers.

First is tacit knowledge; the accumulated manufacturing process understanding, inspection infrastructure, and decades of operating data required to demonstrate 6 sigma reliability simply cannot be extracted from a blueprint or a reverse-engineered component.

Secondly, certified batches of the doped superalloys required for hot section components are sourced from a small number of qualified suppliers whose relationships with the leading manufacturers took decades to build.

Lastly, the precision machine tools required to produce single crystal turbine blades to micron tolerances are themselves a specialized product made by only a handful of manufacturers, with German toolmakers historically prominent among them.

Behind it all sits a century of accumulated operating hours and failure data that the leading manufacturers have built into their design and certification processes. The gap China, for example, faces is having to reconstruct every one of those layers simultaneously.

The terrestrial gas turbines market is similarly concentrated in the Western bloc. Siemens Energy and Mitsubishi Power compete effectively in the heavy frame market alongside GE. The materials demands are less extreme and the certification requirements less stringent but neither Russia nor China has yet produced a competitive large combined cycle turbine without technology transfer or joint venture arrangements with one of the established Western or Japanese leaders.

Russias Gas Turbine woes

The Russian case illuminates what happens when a high-performance industrial capability like gas turbines is simultaneously hit from multiple directions. The deterioration predates the 2022 invasion of Ukraine by decades, beginning with the Soviet collapse and the economic chaos that followed. The engineering talent base that had sustained Soviet aviation and power generation programs dispersed, with experienced engineers leaving for better-paid work abroad or moving into unrelated sectors as defense and industrial budgets collapsed.

The materials problem compounded the talent problem. Russia’s ability to maintain supply relationships for specialized parts, never strong by Western standards, eroded through the 1990s and 2000s as the industrial base contracted.

Then came the precision machining problem. Germany was Russia’s primary supplier of the high-precision machine tools required to produce turbine components to the tolerances modern engines demand. That relationship was embedded in a broader economic interdependence: Russian gas flowing west, German industrial equipment flowing east. Post-2022 sanctions put an end to that special Ost-Politik relationship.

GE’s withdrawal from Russian power generation maintenance under threat of sanctions compounded the crisis at the operational level. GE had engineers on the ground maintaining the most capable turbines running on the Russian grid, many of them originally supplied through the Siemens joint venture arrangements. When those engineers left, the knowledge and tooling they brought with them also disappeared.

The Russian grid is now running aging equipment with a degraded maintenance capability, shortening component life further and creating a compounding reliability problem. Recent adaptations by Russia to overcome sanctions pressure include turning to Iran which has a small but self sufficient gas turbine industry.

The West still dominates. When will the rest catch up?

The gas turbine waited nearly 150 years from theory to practice to join the pantheon of prime movers because the materials and manufacturing precision it required didn’t exist. Its arrival reorganized the world: global aviation, just-in-time supply chains built on air freight, and the most efficient heat engine ever built for generating electricity.

That the Western bloc and Japan still decisively control this technology after nearly a century is the outcome of compounding advantages in materials science, precision manufacturing, tacit institutional knowledge, and certified failure data accumulated across millions of operating hours.

China’s “Two Engines” programme, launched in 2013 and backed by sustained state investment, has not yet closed that gap in either commercial aviation or heavy-frame combined cycle turbines. Whether it eventually does will matter as much to the future balance of industrial power as it does for the semiconductor or battery supply chain contest currently dominating policy attention.

The AI demand surge has arrived into this constrained supply environment with considerable force. CCGT plant costs have roughly tripled over the last 3 years, order books stretch toward the early 2030s, and the gap is being filled in part with jet engines from retired aircraft converted for ground-based power generation. Whether the demand wave will persist long enough to justify genuine capacity expansion, or correct as the 1990s boom did, is the question that manufacturers must judge.

Gas turbines represent an accumulated industrial inheritance which took nearly a century to come within small percentages of theoretical maximum efficiencies. The queue is long in part because the capabilities of those who have mastered the last prime mover are exceptionally rare.

For more on David Helmer visit his website https://www.nttwconsulting.com/

Like this post to keep us pushing the edge of our material limits.

Great article, Chris. I've done a little bit of reading on the metallurgy of modern aircraft engines. It's pretty astounding stuff. This essay is also an interesting contrast to some of your earlier work detailing the engineering and institutional advantages of Russia/China in the nuclear realm, which Western countries forfeited through decades of stagnation. It's heartening to see the opposite scenario with turbine technology.

Wonderful post, Chris.

Perfect mix of history, function, technical challenges, market players and conditions and even how AI is repurposing retired aircraft jet engines to meet the demand. Super.

p.s. Bad idea giving me big ideas about bamboo and gunpower. Otherwise, with the help of my pal the shotgun shell reloader, the neighbor behind me who won't control her bamboo coming across my property line is in for it this 4th of July.

;)