Part 2: The Structural Bull: Why this Uranium Cycle is Different

Supply, Demand, Multipolarity and a more boring Bull Market Ahead?

Recap from last week

The first part of this analysis published last week established why uranium behaves unlike any other commodity: no real-time price discovery, demand that arrives in waves separated by years of buyer silence, and a cyclical pattern sustained across 6 decades by a secondary supply wedge that has now been exhausted.

Today we examine both sides of the ledger simultaneously, because the supply story and the demand story are not independent.

They are pressing against each other in ways the aggregate global supply-demand charts do not capture. The geopolitical fracturing of the market means the relevant question is no longer whether there is enough uranium in the world. There probably is. The question is whether there is enough in the western supply chain, and that is a considerably more uncomfortable place to look

.

What’s structurally different on the supply side

The absence of secondary supply changes the mathematics of the uranium market in a way that has not yet been fully priced into conventional analysis. When the next demand surge arrives, there is no inventory wedge to release.

The price signal that would previously have been dampened by a flood of government stockpile material or down-blended warheads will now have to travel all the way to primary producers, who will have to respond by sinking capital into new mines that take years to permit, build, and bring to full production. That lag between price signal and supply response is the structural feature that distinguishes this cycle from every predecessor.

Cameco’s position within that structure is deliberate. The company still has 30% of its licensed, permitted production capacity either in care and maintenance or operating below full rate, held in reserve explicitly because sufficient long-term contracting has not yet arrived to justify restart. Isaac was direct about this: there is no build-it-and-they-will-come model in uranium.

Producers commit capital after securing forward demand, not before. Cameco’s Millennium deposit and other Athabasca-adjacent assets remain in the ground as inventory, pounds with a balance sheet value that appreciates as the price environment improves, available for development when the contracting signal justifies it. The discipline is a deliberate strategy of matching production decisions to marketing outcomes rather than running mines at capacity and hoping the market absorbs the output.

Kazatomprom has arrived at the same position by a harder road. Having learned during the post-Fukushima bear that maximizing volume destroys the value of the national asset it is supposed to steward, Kazakhstan’s state producer now runs a contracting-first strategy that mirrors Cameco’s. The production target reductions that initially looked like a sulfuric acid supply problem, output guidance cut 10 to 15% at first and now closer to 25%, are better understood as a capital allocation decision dressed in operational clothing.

The sulfuric acid shortage is real with phosphate fertilizer production competing for available supply, and the constraint genuinely biting into production volumes that Kazatomprom had already sold forward. Building a new sulfuric acid plant takes 18 to 24 months and costs $200 to $300 million. Kazatomprom has done exactly this before and the engineering knowledge exists.

The decision to fund and begin construction came as contracting conditions improved through 2023, not at the moment the shortage first appeared. The plant is now under construction and expected online in 2026. That it was conceived and financed alongside a strengthening contract book, rather than purely in response to an operational emergency, is the tell.

What settles the supply discipline question is Kazatomprom’s 2026 guidance, which has nothing to do with acid. The company announced a further roughly 10% production cut for 2026, stating explicitly that current prices and the existing level of uncovered demand are not sufficient to incentivise a return to full output.

New Athabasca Basin development offers genuine upside against this tightening but carries first-of-a-kind risk that promotional materials for junior developers tend to understate. NextGen Energy’s Rook One project anticipates production of around 30 million pounds per year, which would be transformative for the western supply picture if it materializes on schedule.

But Cigar Lake’s mining method was built on decades of institutional accumulation by a company that had already operated McArthur River and learned the hard way what fractured sandstone and unconformity-hosted ore bodies do when water management fails. The freeze engineering, the jet-boring system, the radiation handling protocols for 15% ore grades: none of this existed as received knowledge before Cameco developed it.

A new operator in a different geological setting, without that institutional base, faces engineering challenges with no established playbook. Isaac described the dynamic precisely: junior uranium projects tend to attract elevated valuations before they have entered what he called the valley of development, the long and capital-intensive period between exploration promise and operational reality.

Cameco’s own reserve and resource pipeline contains around one billion pounds, all adjacent to existing infrastructure and already on the balance sheet. Any external acquisition has to clear that internal hurdle rate. At current junior valuations, very few external projects do, and the moment when they will is the moment those projects have moved through the valley and been repriced accordingly. There is a significant incumbent advantage.

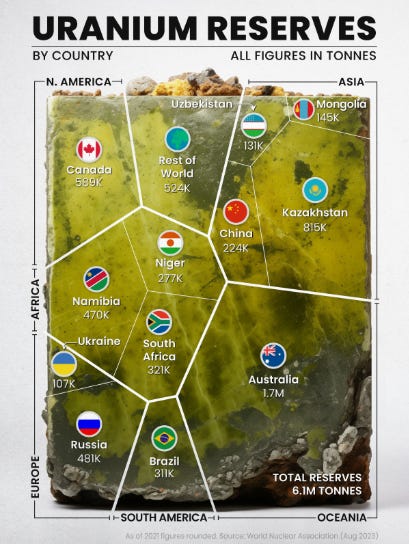

The geopolitical dimension of the supply picture adds a further layer of tightening, one that aggregate global supply-demand charts tend to obscure entirely. Uranium has always been a highly trade-dependent commodity; for most of the industry’s history, around 90% of uranium production came from countries with no civilian nuclear power program, while around 90% of demand came from countries with little or no domestic uranium production. The system worked because no one worried much about where the uranium came from. The unipolar exception to the rule made that comfort possible. Emerging multipolarity is challenging what in retrospect was a naive assumption.

Multipolarity and a fracturing market

The standard supply-demand analysis of the uranium market operates at the global aggregate level: total pounds produced, total pounds consumed, projected deficit or surplus. That framing was adequate for a world in which uranium flowed freely across borders toward whoever offered the best price and utilities had no preference for origin. That world is gone, and the aggregate framing now obscures more than it reveals.

The uranium market is splitting into two increasingly separate procurement spheres. On one side sit US, European, Japanese, and South Korean utilities buying uranium that can pass ESG screens, government security reviews, and shareholder scrutiny.

On the other sit Chinese state enterprises and Rosatom export clients building reactors and fueling them through supply chains largely invisible to western price reporting and largely inaccessible to western buyers. The question that matters for uranium investors is not whether there is enough uranium in the world. There probably is. The question is whether there is enough in the western supply chain, and that is an increasingly different and more uncomfortable question.

China’s nuclear ambitions alone reframe the demand picture in ways the aggregate numbers do not capture. China currently operates around 62 reactors and has roughly 34 more under construction, with stated government targets pointing toward 150 GW of installed capacity by 2035, roughly triple today’s fleet. That uranium demand is being served through a supply architecture running parallel to the western term market: bilateral offtake agreements with Kazakhstan and Uzbekistan, African production assets acquired by Chinese state enterprises, and processing arrangements that often route material through Russian infrastructure. None of this volume shows up in western spot or term prices as demand. It disappears from the pool of available western-origin supply without generating a visible price signal in the markets western investors watch.

The ownership map of global uranium production makes this dynamic more acute than the geography suggests. Kazatomprom is state-owned. Uranium One, which holds significant Kazakh production stakes, is owned by Rosatom. CNNC controls Rössing in Namibia, with output largely committed to Chinese offtake, and Husab, also among Namibia’s larger producers, is similarly Chinese-controlled.

Namibia looks like a western-friendly source until that ownership layer is examined. Niger’s Somair mine was effectively removed from the western supply chain by the 2023 coup. The geographic map of uranium production and the geopolitical map of uranium availability are not the same map, and confusing them produces dangerously optimistic supply assessments.

The spot and term prices that western investors watch are prices in the western procurement sphere. As western-origin supply tightens relative to western demand, those prices will increasingly reflect western-origin scarcity rather than global aggregate adequacy. The fracture is not symmetric, and the side bearing the greater adjustment cost is the side that spent the post-Cold War decades assuming global commodity markets were a permanent and neutral feature of the energy landscape.

What’s structurally different on the demand side

The demand transformation driving this bull has two distinct layers that are worth separating before examining how they interact. The first is the reversal of the post-Fukushima western phaseout. The second is a class of demand that did not exist in any previous uranium cycle. Together they are pressing against a supply base that is simultaneously tightening for the structural reasons described in the previous section.

Russia’s invasion of Ukraine in February 2022 was the demand-side inflection point. Before the invasion, energy security was a minor consideration in power planning; after it, energy security became the dominant concern. Nuclear’s profile changed accordingly. A technology that was sunsetting as a legacy baseload asset in increasingly deregulated western grids was suddenly being re-examined as a mature, dispatchable, carbon-free power source that does not depend on fuel imports from geopolitically unreliable suppliers.

The irony that Russian enrichment services remained deeply embedded in western fuel chains long after the invasion made the point more viscerally than any policy paper could. Belgium reversed its phaseout. Japan began restarting reactors that had sat idle since 2011, with a government target of returning 30 or more units to service. The United States passed legislation extending production tax credits for existing nuclear plants and strengthening support for new construction, while several European governments that had treated nuclear as a managed decline reclassified it as critical infrastructure.

The reactor life extension wave matters enormously for uranium demand because it converts what had been scheduled demand destruction into sustained long-run consumption. A reactor expected to retire in 2030 that instead receives a subsequent license renewal to 2050 adds 20 years of uranium conversion, enrichment, and fabrication demand. Given the relatively small fleet of global reactors, each reactor is individually responsible for roughly 0.2% of global demand. Multiplied across the US fleet, where subsequent license renewals are now the norm rather than the exception, and across Europe and Japan, the aggregate addition is substantial.

Roughly 70 reactors are currently under construction globally, a figure not seen since the 1970s construction wave, and the uranium demand from those reactors is being contracted years before the plants begin operating. The contracting signal is already building in the term market even though the physical consumption is still years away.

Then there is the data center and artificial intelligence demand signal, which did not feature in uranium investment theses as recently as three years ago. Microsoft’s agreement with Constellation Energy to restart Three Mile Island Unit 1, Amazon and Google signing nuclear power purchase agreements, and a broadening field of technology companies explicitly seeking firm 24-hour carbon-free baseload to power compute infrastructure have introduced a class of buyer into the nuclear power market with no historical precedent.

These buyers carry deep balance sheets and a demonstrated willingness to sign long-duration contracts to secure power supply certainty, and their demand is structurally incompatible with intermittent generation: a data center cannot tolerate the output variability of wind and solar without storage infrastructure that does not yet exist at the required scale and cost. Nuclear is the only mature technology that satisfies both the carbon and the reliability constraint simultaneously. The data center signal is still early but it is layering onto an already tightening picture rather than driving it independently.

The procurement sequencing laid out in Section 1 gives a precise read on where western utilities currently sit within all of this. Conversion prices are at historic highs; the western conversion market, dominated by Cameco’s Port Hope facility and Orano’s Metropolis Works, has essentially no spare capacity and is fully contracted well into the next decade.

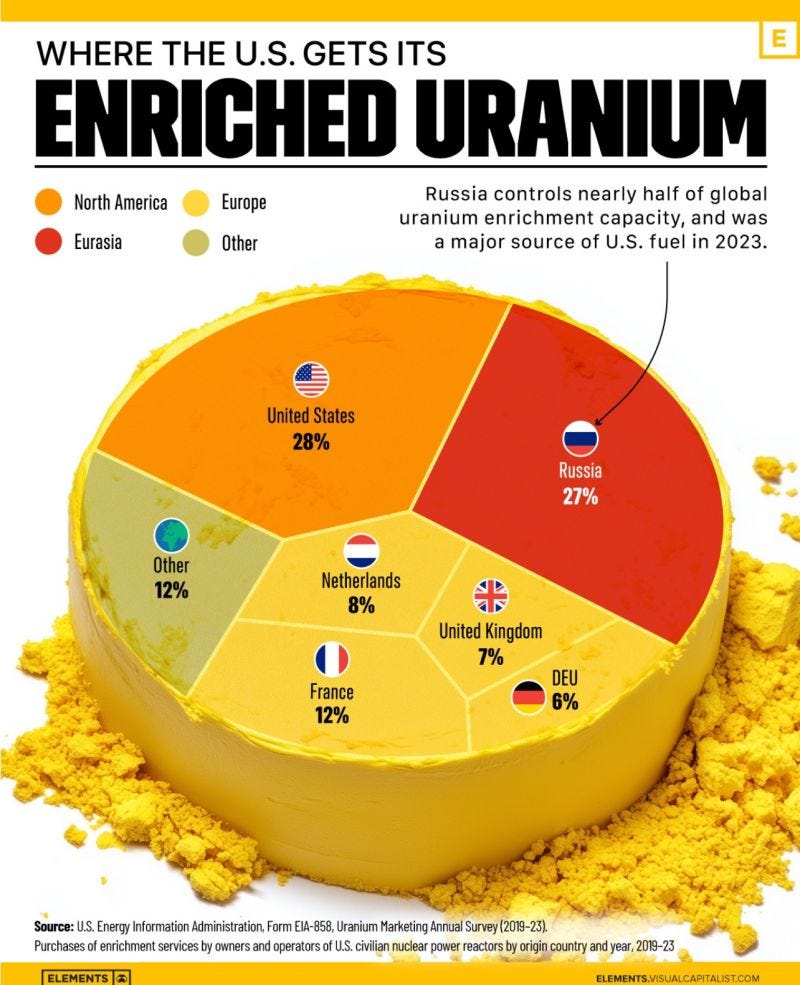

Enrichment is similarly tight: after the effective sanctioning of TENEX, Russia’s enrichment export arm, western utilities were left with Urenco and Orano as their primary options, both running at high utilization, and new enrichment capacity takes 10 or more years to permit, finance, and construct. Fabrication contracted, enrichment contracted, conversion contracted. The uranium contracting wave has not yet fully arrived. When it does, it will hit a primary supply base deliberately held in partial restraint, with no secondary supply available to buffer the price signal.

What Cameco’s Vertical Integration Signals

Cameco’s growing vertical integration spans the full western nuclear fuel cycle by design. The 1988 merger of two Canadian Crown corporations created a company that ran from Athabasca Basin mining through milling, refining, and CANDU fuel fabrication from the outset. What has changed over the subsequent three decades is the deliberate extension of that integration into the light water reactor fuel cycle, which accounts for roughly 92% of the world’s operating reactors, culminating in the Westinghouse acquisition completed with Brookfield Asset Management in 2023.

That acquisition is best understood as demand creation. Between what Cameco handles for pressurized heavy water reactors and what Westinghouse handles for light water reactors, around 65% of western world fuel bundles pass through a facility owned by one of the two companies. Every AP1000 that Westinghouse sells and builds is 80 to 100 years of upstream demand for uranium, conversion, enrichment, and fabrication. The logic is circular in the most productive sense: building reactors creates the long-run demand that justifies investing in the upstream supply chain to serve them.

In the fracturing market described in the previous section, Cameco’s ownership structure is itself a competitive asset in a way it was not a decade ago. Western utilities under government pressure to demonstrate supply chain security are not indifferent to the fact that a long-term contract with Cameco is a contract with a Canadian-domiciled, privately owned company whose assets sit in Saskatchewan and Ontario, jurisdictions with stable rule of law and no plausible scenario in which production gets diverted to a state strategic priority. That provenance premium is real and growing as geopolitical sorting accelerates.

Cameco’s Athabasca Basin operations rest on institutional knowledge that cannot be acquired quickly regardless of capital availability: freeze engineering, jet-boring protocols, radiation management at ore grades with no parallel elsewhere in the western world. That knowledge lives in a small workforce operating in one of the most remote industrial environments on the planet, and it is not easily replicated. NexGen and Denison are competing for the same scarce pool of experienced operators and engineers that Cameco has spent decades cultivating.

The labour market in northern Saskatchewan is not elastic. You cannot import this expertise from a copper mine or a conventional uranium operation in Kazakhstan or Namibia. The tacit knowledge embedded in Athabasca Basin operations is specific to that geology, that ore grade, and those extraction methods, and it accumulates slowly through direct experience rather than capital deployment.

Each new deposit presents its own first-of-a-kind engineering problem: McArthur River and Cigar Lake sit 55 kilometres apart and require fundamentally different extraction strategies, and there is no reason to expect the next generation of deposits present less novel mining engineering challenges.

The physical moat and the human capital moat reinforce each other. These barriers do not appear on a balance sheet, but they are the reason Cameco’s assets command the strategic premium they do, and they are the standard against which junior developer promises should be measured.

The company with the deepest operational knowledge of western uranium supply and the most granular view into western utility contracting is the one holding 30% of its licensed capacity in reserve, waiting for the long-term contracting signal to fully arrive. That patience is the clearest available signal that the uranium bull has not yet reached the point at which the smart money feels compelled to rush.

A more boring bull market, maybe

The long-term uranium contract price has been moving steadily upward for three years without a significant reversal, grinding methodically in one direction rather than spiking on a single supply shock or sovereign buying program the way previous bulls did.

That grinding reflects something no previous uranium bull possessed: two major incumbent producers running explicit supply discipline simultaneously, no secondary supply available to buffer a demand surge, a geopolitical environment pushing western utilities toward a narrower pool of origin-appropriate suppliers, and a demand base being rebuilt on foundations more durable than a single policy announcement.

The structural conditions for a disorderly blow-off top, the pattern that ended every previous uranium bull, are less present in this cycle than in any prior one. Kazatomprom now understands that flooding the market destroys the value of a national asset it cannot replace. Cameco has demonstrated through a decade of curtailments and patient contracting that it will not produce into a weak market.

The secondary supply shock absorber that historically amplified both the upswing and the collapse is gone. And the geopolitical fracturing of the market means a Kazakh production surge is less likely to land in the western spot market than it would have in 2012, because the offtake architecture routing Kazakh material toward Chinese and Russian end users is now more contractually entrenched and more politically durable than it was during the last bear.

The residual tail risks are real. A nuclear accident remains the industry’s defining vulnerability, though it would now be in a world where climate security, energy security, and national security have become the explicit pillars of power sector planning in every major western economy.

Governments that reversed phaseout decisions on energy security grounds are less likely to reverse course again, and the generation of reactors now operating embody safety improvements that make a Fukushima-scale event substantially harder to replicate.

The more immediate uncertainty is timing. The uranium market ultimately depends on utilities bringing forward demand, and that timing is not controllable by producers. Conversion and enrichment contracting already reflect the tightened supply picture.

When uranium contracting fully catches up, the price signal will reach producers holding capacity in reserve for exactly that moment. Whether that resolves in an orderly repricing or a violent catch-up move depends on how quickly the last domino falls and how much new primary supply can be brought online in response.

What this cycle has that its predecessors lacked is a structural foundation underneath that uncertainty and that is what makes it worth understanding on its own terms.

Like this post to help balance supply with surging demand for Decouple Media content.

The coming uranium supply crunch will add importance to Global Laser Enrichment of the very large supply of U235-depleted uranium already stored as UF6. Chloride molten salt fast reactors are another way to use that extensive fuel source. Terrapower used to work on this, but there are no recent updates. I bet the 'salt' engineer were transferred to Atrium's molten salt heat storage project. Other possible competitors include Copenhagen Atomics.

Many thanks for this a good read. Any thoughts on the investment case for Kazatomprom ?