LNG’s Weak Link

The Fuel That Flipped the Risk

There is a structural reason that explains the paradox of the unique vulnerability of LNG, as illustrated by the force majeure of Qatar’s Ras Laffan, and the historic attractiveness of the fuel to importing countries.

The complexity of conventional oil sits at the importer’s end in multi-billion dollar refineries which take years to build.

LNG is almost the opposite: its complexity sits at the exporter’s end, locked inside exquisitely engineered liquefaction infrastructure. On the importer’s side warming the liquid back to its gaseous state requires little more than running seawater over a heat exchanger.

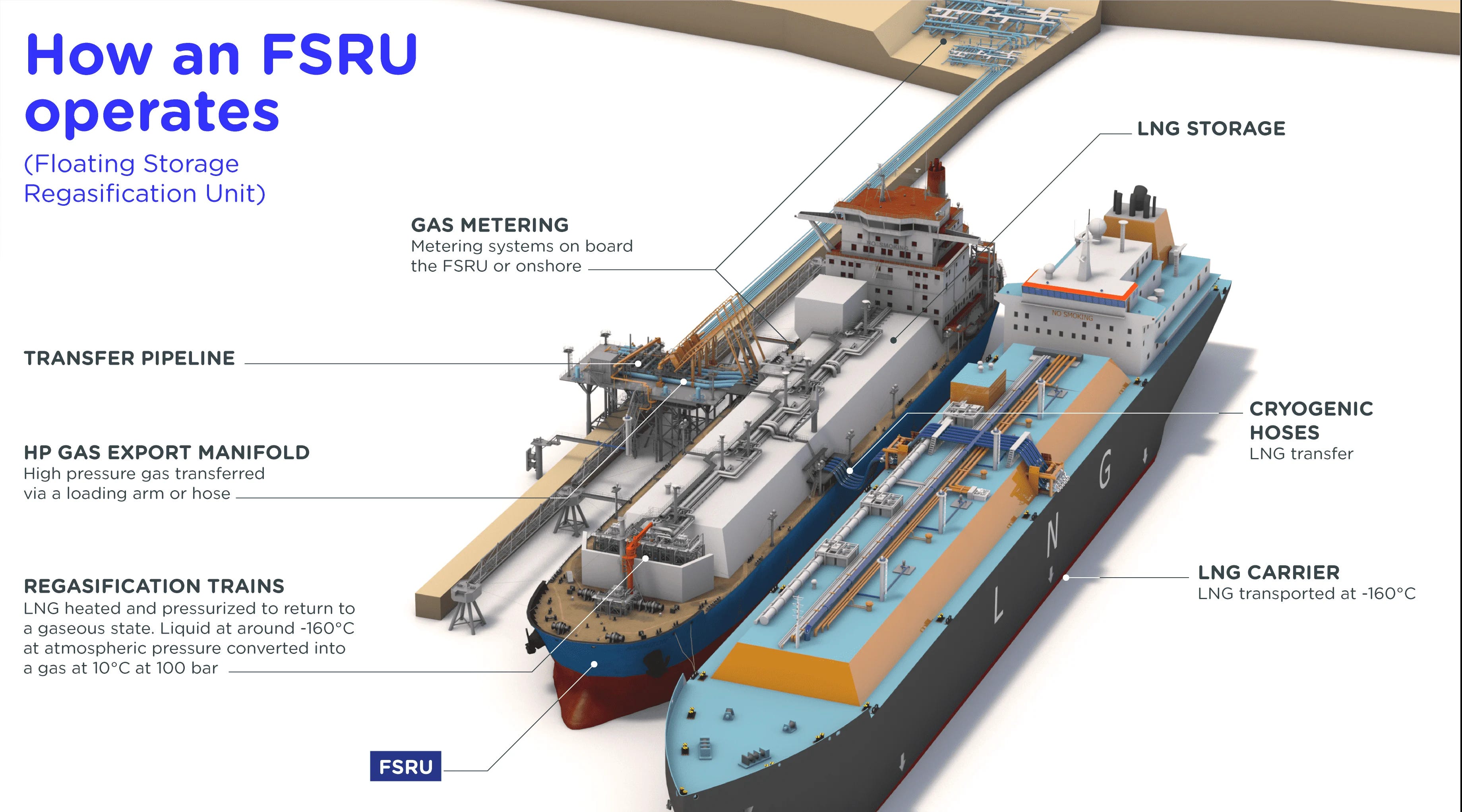

The Germans demonstrated this at breakneck speed during the energy crisis of 2022. They built 5 floating storage and regasification units, essentially modified LNG tankers moored offshore. The fastest was stood up in under seven months.

Once regasified the pressure is managed, a pipeline is run to a combined cycle gas turbine, and voila you have electricity. Those power plants are assembled in 24 to 36 months from factory-built components with very low construction risk. They achieve close to 60 percent thermal efficiency, making them the most thermodynamically elegant large-scale power plants ever constructed.

The complexity on the production side is a different matter entirely. Each liquefaction train at Ras Laffan represents roughly $7 billion in capital investment. The process reduces its volume by roughly 600 times through cryogenic cooling, getting it down to the minus 162 Celsius threshold where it occupies a manageable volume for ocean transport.

This is the asymmetry that explains why so many countries made what seemed like rational energy security bets on LNG. The capital burden on the importing side was manageable and the long term contracts relatively affordable. Supply during an era of open sea lanes and reliable contracts, looked stable.

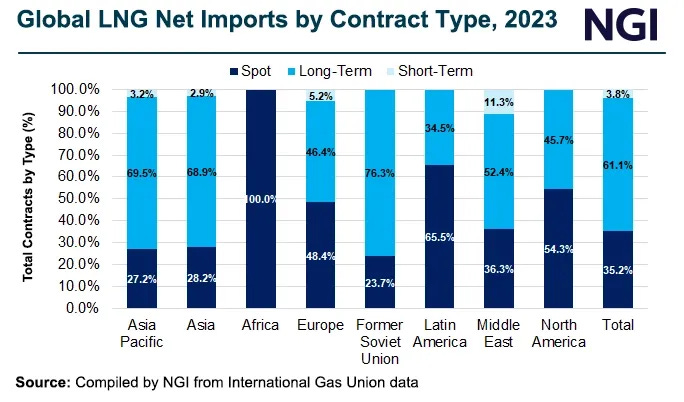

Unlike crude oil, where pricing is anchored to deep, globally traded benchmarks and a highly liquid spot market, LNG remains structurally tied to long-term bilateral contracts necessary to cover the high capital cost of liquefaction facilities.

Today roughly 60% of global LNG volumes are committed under such contracts, leaving a relatively thin pool of uncontracted supply. Most cargoes are pre-allocated, so a country reliant on Qatari volumes cannot readily switch to Australian or U.S. supply at short notice. In a global supply crunch these buyers are pushed into the spot market, where competition for a relatively thin pool of uncommitted cargoes drives prices sharply higher.

Even as the U.S. brings new liquefaction capacity online, LNG supply remains slow to adjust. New trains are costly and can take close to a decade from initial planning to first cargo, leaving limited spare capacity to absorb sudden disruptions.

The 2022 European gas crisis offered a deceptive lesson. Germany solved it by building receiving infrastructure fast, which made LNG look resilient. That was however an importing problem, not a production problem. Global liquefaction capacity was intact and US production was surging. The receiving end of LNG bends to political will, tight timelines and emergency permitting. Destroyed liquefaction infrastructure does not.

Excellent article. I just subscribed.

LNG is often viewed as a global commodity with elastic supply & demand curves. However, the reality of LNG is much different.

When disruptions occurred to the global LNG supply chain, the system responds by re-allocating existing supplies or reducing demand. This is why LNG markets do not provide good shock absorption capabilities. In addition, they can make many of these shocks worse.

This is also where I think most of the market based models fail. Most models treat price as an adjusting variable. However, for LNG, the primary constraint on the system is throughput, not price. When such constraints cause adjustments via reductions in demand rather than expansions in supply. The impacts create pressures on inflation rates, create constraints for policymakers & result in tighter liquidity across the entire system.