Fission Impossible? Financing New Nuclear

In much of the West, what is holding back nuclear power is no longer safety concerns, regulation, or public opinion.

In America, despite eye watering subsidies and incentives, utilities just aren’t biting. The question that dogs future nuclear projects is not just how to raise substantial amounts of capital: it is who will absorb the risk of construction overruns.

Like hydroelectric dams, nuclear reactors take the better part of a decade to build, and across that whole period consume enormous amounts of capital while generating no revenue.

The interest accumulated during construction compounds on itself year on year. As a result, depending on the cost of capital and adherence to schedule, by the time first electricity is sold, the financing cost can dominate everything else.

A combined-cycle gas turbine serves as a useful counterpoint and explains why one technology attracts private money and the other repels it.

A gas plant is predictably constructed in 18-30 months, drawn from a module supply chain that reliably ships hundreds of units a year. Interest during construction doesn’t have time to balloon, and as long as there is demand to serve the asset begins earning revenue quickly.

As a result fixed-price contracts have been commonplace, which is why merchant developers finance gas plants privately without a second thought.

A nuclear megaproject carries two major financial risks. The first is construction risk: will the plant be built on time and on budget? The second is offtake risk: once the plant exists, will a customer pay enough across 60 to 80 years to service the debt?

Nuclear financing structures are fundamentally arrangements for distributing those two risks among a fixed cast of parties that includes the reactor designer, the construction firm, the utility, the government, the ratepayer, the taxpayer, and the industrial offtaker.

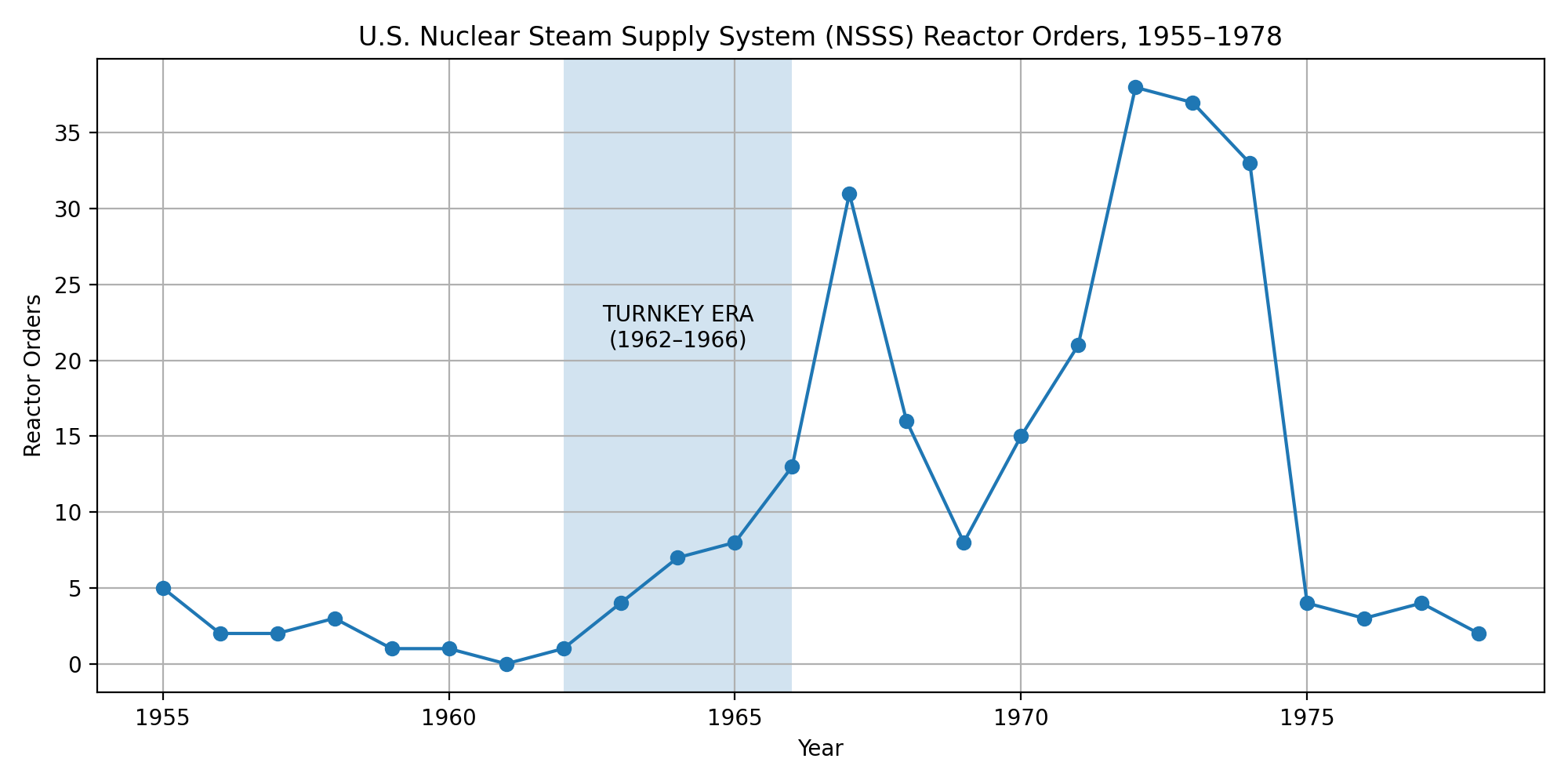

Initially, to launch the industry in the USA in the early 1960s GE and Westinghouse took on all construction risk and delivered 13 loss-leading plants under fixed price contracts.

They successfully scaled reactors to sufficiently viable economies of scale that regulated monopoly utilities, confident after a building spree of conventional thermal plants, took on the construction risk. Offtake risk was minimal as electricity demand was skyrocketing in the 1960s.

They financed projects against a captive ratepayer base which offered a low cost of capital. Prudent costs could be passed on to the ratepayer and there was little downside to shareholders.

Elsewhere around the world the answer to the question of who takes on the risk lay with government-owned utilities backed by ratepayers and ultimately taxpayers.

France’s EDF, Ontario Hydro, and Korea Hydro & Nuclear Power could borrow at or near sovereign rates because the lender was, in effect, lending to a government. In these scenarios, nuclear power was being built and financed like infrastructure rather than merchant generation.

In the fizzled “Nuclear Renaissance” of the early 2000s Europe and America tried a variety of approaches to finance EPR and AP1000 reactors.

In the accompanying Decouple Podcast interview with Michael Seely we analyze the evolving state of nuclear construction finance with a deep dive into EPR projects in Finland, France and the UK and look towards what optimal arrangements will look like in the nuclear builds of the future.

Another good episode. However, I would disagree with the remarks about TVA's ability to finance nuclear plants. In the 1960s and early 1970s TVA started construction on 17 nuclear units. Only 7 were finished and currently operate. Due to the prolific spending, Congress in 1979 set a statutory debt ceiling of $30 billion. Currently TVA has a debt of roughly $23.8 billion.

If the debt ceiling was adjusted for inflation today it would be roughly $138 billion.

The cost estimate for the Clinch river BWRX-300 is $5.4 billion. DOE is kicking in a $400 million dollar grant. Unless some other financing mechanisms are used this will project will bring TVA very close to the debt ceiling.

Seems like the future of Nuclear is via SMR’s. These large projects carry too much uncertainty as you noted. Thats where the capital is flowing so that cost is predictable and scalable.