Canada’s Most Undermarketed Industrial Asset Is Finally Getting Its Sales Pitch

AtkinsRéalis’ Joe St. Julian makes the case that Canada is closer to a fleet build than most people realize.

Joe St. Julian arrived at AtkinsRéalis four years ago as an outsider. He had spent two decades at Bechtel, most of it in the American federal nuclear sector, running cleanup operations at the K-25 gaseous diffusion facility in Oak Ridge, then serving as project manager on the Hanford Waste Treatment Plant, the $25 billion vitrification facility built to immobilize the liquid plutonium production waste accumulated between 1945 and 1987. Before that he had built large combined-cycle gas plants in Michigan for the Shaw Group. He is, in other words, a construction and project controls man who spent his career in the most complicated industrial environments the American government could devise. He did not grow up in CANDU.

That background turns out to matter for what he had to say about it. When St. Julian arrived in Canada and started doing what he calls “due diligence” on the reactor technology he had just been hired to sell, he was surprised. “I was actually shocked,” he told me. “I thought it was an incredibly innovative technology.”

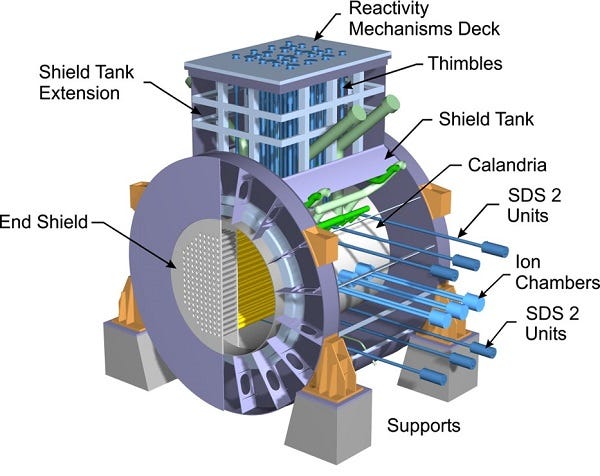

American nuclear culture produced four original equipment manufacturers whose light water reactor designs account, directly or indirectly, for the vast majority of the world’s operating fleet. Canada went a different direction entirely. No enrichment dependency, no large forged pressure vessel, a reactor that runs on natural uranium and refuels online without shutdown. Thirty-five units built across six countries with a further 18 CANDU inspired pressurized heavy water reactors built by India. Almost nobody outside those countries can describe how it works.

St. Julian’s diagnosis of that invisibility is blunt: if the same technology had been developed in the United States, everyone in the world would know about it. He frames it as a cultural gap rather than a technical one. Canada built something genuinely differentiated and then, with characteristic understatement, did not particularly insist that anyone notice.

The last new CANDU to enter commercial service was Cernavodă Unit 2 in Romania, in 2007. Almost twenty years have elapsed since then, and the Canadian domestic fleet has been in a sustained refurbishment cycle rather than a new-build cycle. That refurbishment program, covering units at Darlington and Bruce Power in Ontario, has been ahead of schedule and under budget. St. Julian argues that the refurbishments are the most important thing that has happened to the CANDU program in the last two decades because they generated the operational knowledge, supply chain capacity, and cost data that a new-build program requires.

The Metamorphosis of the Monark

The product AtkinsRéalis is now offering domestically is somewhat confusingly called the “Monark.” When AtkinsRéalis unveiled the Monark at the World Nuclear Exhibition in Paris in November 2023, the company broke with CANDU’s naming conventions entirely. Where previous designs had carried alphanumeric designations tied to their fuel channel count or development lineage, the Monark was positioned as something categorically new: a 1,000 megawatt single-unit design drawing on civil infrastructure of two designed but never built CANDU designs, the ACR-1000, the EC6, as well as the reactor core of the Darlington station, with CANDU’s passive safety features and a 70-year design life. Its marketing emphasized a break from the past.

That concept has since been substantially reoriented. What St. Julian described in our conversation is a configuration being referred to as the Monark-D, for Domestic. It consists of a strict four-unit replication of the Darlington station as it stands today, refurbished and relicensed, with as few material design changes as possible. The driver has come from the utilities who are becoming increasingly gun shy about first of a kind (FOAK) risk. That risk is increasingly being seen as the primary killer of nuclear cost and schedule. The way to bound it is to build what has already been licensed.

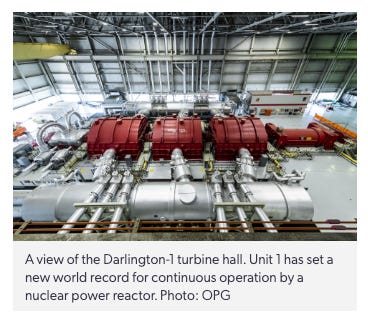

The confidence for replicating Darlington comes from its excellent operating experience and the confidence of the regulator. Darlington Unit 1 holds the world record for the longest continuous run of any thermal generating plant in history, 1,106 consecutive days, a figure made possible by CANDU’s online refuelling capability, which allows fuel replacement without shutdown.

The CNSC granted Darlington a 20-year operating licence in September 2025, the longest nuclear operating licence ever issued in Canada, following the completion of a C$12.8 billion refurbishment that finished four months ahead of schedule and C$150 million under budget.

The four-pack configuration matters economically: shared containment, a single control room, shared utilities, all of which pull the capital cost per megawatt below what any single-unit arrangement can achieve, which is partly why Ontario’s utilities have built this way since Pickering.

The Domestic CANDU Market

The near-term domestic pipeline St. Julian described is large. Bruce C, a four-pack on the Bruce Power site. Wesleyville A and potentially Wesleyville B, totalling another eight units east of Toronto. That is twelve reactors in Ontario alone, all potentially Monarks. Getting there requires first validating that the Darlington design, as built, can be crosswalked to current codes, standards, and regulatory expectations without requiring changes expensive enough to undermine the economics.

AtkinsRéalis is currently working through approximately 400,000 design documents: calculations, drawings, specifications, studies and re-stamping each one against today’s engineering standards with a professional engineering seal. The CNSC has identified 7 licensing areas out of a total of 18 that require examination given the evolution of codes since Darlington was originally licensed roughly forty years ago.

The three that St. Julian flagged as most technically involved are seismic criteria, aircraft impact requirements introduced after the September 2001 attacks, and the instrumentation and control (I&C) architecture, which mixes analog and digital systems in ways that must be demonstrated adequate against current safety standards.

On each of these, St. Julian’s position is that there are no fundamental licensing barriers, a term he was careful to distinguish from “no issues.” Fundamental barriers, he explained, are a concept that applies to genuinely novel reactor designs, where some core aspect of the physics or safety case has never been reviewed by a regulator.

CANDU has thirty-five operating units and a safety record the CNSC knows in detail. The question is not whether it is licensable. The question is whether satisfying any evolved requirements will require material changes expensive enough to shift the levelized cost of electricity (LCOE) beyond what Ontario’s utilities and ratepayers can absorb. AtkinsRéalis expects to have answers by the third quarter of 2026.

What will it cost?

While refusing to offer an on the record estimate, St. Julian’s core point is that repetition drives the marginal cost down, and CANDU has more repetitions behind it than any of its Western competitors in the current market. The AP1000 has two operating units at Vogtle in Georgia, and four in China with twelve currently under construction there.

The EPR has Taishan 1 and 2 in China, Olkiluoto 3 in Finland, Flamanville in France and Hinkley Point C still under construction in the United Kingdom.

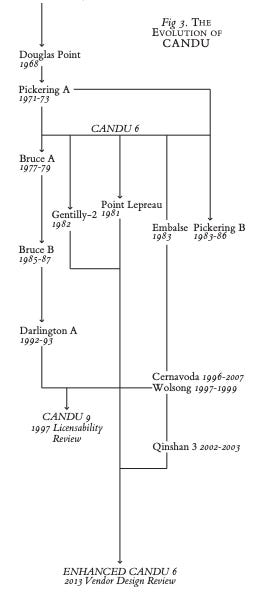

There have been 35 CANDUs built but the raw global count is not the most telling number for the Monark-D specifically. The four-pack configuration that Darlington replicates has been built five consecutive times in Ontario alone: Pickering A, Pickering B, Bruce A, Bruce B, and then Darlington itself, twenty large multi-unit reactors in sequence, each generation absorbing the lessons of the last.

The Darlington units are effectively the 17th through 20th iterations of that configuration. The wrinkles accumulated across Pickering and Bruce, the steam generator designs, the I&C architecture, the containment geometry, the shared utilities layout, were progressively reworked before shovels broke ground at Darlington.

St. Julian was pointed about what this means for comparative LCOE calculations against competitors like Westinghouse now attempting to ramp the AP1000 from its 35 billion dollar cost for unit 1 & 2 at Vogtle to serial three: “I can’t reduce the cost from serial two to serial three by 50%. It can’t be done. It’s never been done in the history of the world.”

The refurbishment data reinforces this. The first Darlington unit to go through its mid-life refurbishment took 44 months from October 2016 to June 2020. Unit 4, completed in March 2026, was done in 968 days, roughly 32 months, four months ahead of its own schedule. From the first refurbishment to the last, the outage duration compressed by roughly 30 percent. The overall C$12.8 billion program landed C$150 million under budget.

The new-build Monarks are being designed with a 35-year initial licensed life rather than 30, and St. Julian projected that the first life extension following that period will cost roughly half what the Darlington refurbishments did, because the institutional knowledge will already exist in the supply chain and the workforce. A hundred-plus year asset with two economic life extensions, not a 35-year asset followed by a decommissioning decision.

The CANDU Export Market

Romania

The two CANDUs with the most direct bearing on international sales prospects are not in Canada. They are at Cernavodă in Romania. Four stand alone CANDU 6 units began construction there in the 1980s but were interrupted by the fall of the Ceausescu regime. Units 1 and 2 have been in operation since 1996 and 2007 respectively. However AtkinsRéalis is now under contract to finish the partially built Units 3 and 4 at the same site. The C6 design, 380 fuel channels, 730MW output, already licensed in Romania and certified by the European Union, is the product AtkinsRéalis is leading with in Eastern Europe.

Poland

Poland is the most advanced conversation. St. Julian and AtkinsRéalis CEO Ian Edwards were in Warsaw recently for a supplier day intended to introduce the CANDU supply chain to Polish industrial partners. Export Development Canada (EDC), the federal export credit agency, has received a request for $15 billion in financing support on the basis that Polish units would generate at least that much in Canadian content.

For context, the EDC committed $850 million in loan guarantees to the Cernavodă Unit 1 life extension and $3 billion to finish the partially built Units 3 and 4; AtkinsRéalis is currently revising that latter application upward to $4.5 billion as the front-end engineering design matures and Canadian content projections improve.

The pattern in these deals is consistent: EDC provides a low-interest sovereign loan to the buyer country, the contractual requirement for Canadian content means the money flows back into Canadian engineering firms and manufacturers, and the loan is repaid from electricity revenues over the life of the plant.

Turkey and Asean

Turkey is the other active conversation in Eastern Europe, somewhat further behind Poland. The Association of Southeast Asian Nations (ASEAN) countries represent a cluster of longer-horizon opportunities: St. Julian said AtkinsRéalis is in discussions with six of the eight or nine ASEAN members, none of which currently have nuclear power and all of which have begun developing domestic regulatory capacity.

China

China is the most complicated file. Canada has had a continuous presence there since the two CANDU 6 units were built at Qinshan Phase III, commissioned in 2002 and 2003 by AECL on a turnkey basis, on schedule and under budget by a team led by legendary project manager Ken Petrunik. Those units are entering refurbishment planning and early-phase execution through TQNPC (Third Qinshan Nuclear Power Company). Qinshan’s CANDU units are consistently among the top-performing reactors in China by capacity factor and reliability, with periods where they rank at or near the very top of the national fleet.

There were preliminary discussions about building two additional C6 units in part to boost China’s endogenous medical isotope production, over 80% of which occurs at the existing Qinshan units, before the geopolitical deterioration of Canadian-Chinese relations in the late 2010s closed them down.

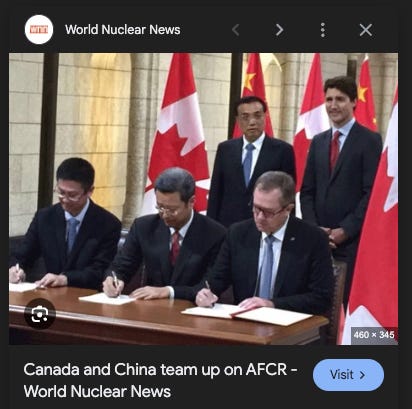

The Advanced Fuel CANDU Reactor

The more technically interesting conversation concerns the Advanced Fuel CANDU Reactor (AFCR), a concept developed jointly by Candu Energy, CNNC, TQNPC, the Nuclear Power Institute of China, and China North Nuclear Fuel Company through a series of agreements from 2005 to 2016.

When a PWR discharges spent fuel, that fuel still contains roughly 0.9 percent uranium-235, compared to the 0.7 percent in natural uranium that CANDU was designed to burn. A PWR cannot reuse that material directly because even at the higher enrichment levels that went in, the discharged concentration is too low to sustain a PWR chain reaction. The uranium must first be recovered through conventional reprocessing, which chemically separates it from the fission products and plutonium accumulated during irradiation. That recovered uranium is then blended down with depleted uranium from enrichment tails to produce what the program calls Natural Uranium Equivalent fuel. Because CANDU’s high neutron economy can sustain a chain reaction at concentrations that would extinguish a PWR, this blended fuel feeds into a CANDU core without any re-enrichment.

The ratio the joint development work confirmed is 4:1: the spent fuel from four 1,000 megawatt PWRs can fully supply one 700 megawatt AFCR, extracting a further 30 to 40 percent of the energy remaining in that material, while simultaneously drawing down the stockpile of depleted uranium enrichment tails used as the diluent, a stream that is itself an expensive long-term storage liability accumulating at enrichment facilities worldwide. The detailed conceptual design was completed and the fuel technology was partially demonstrated at Qinshan. Twenty four NUE bundles were successfully irradiated in the demonstration program, however NUE fabrication remains an open engineering problem, with pellet sintering challenges that have so far required a more involved powder conversion process. Ultimately the political rupture in Canada-China relations ended the program.

To grasp why this matters to China specifically, consider the trajectory. China currently operates around 58 reactors totalling roughly 60 GWe, with 33 more under construction and credible projections putting the fleet at 300 GWe or beyond by 2050. China already imports 80 to 85 percent of its uranium requirements; at 300 GWe of predominantly PWR capacity, annual uranium demand would approach 50,000 tonnes in a global market that produced around 60,000 tonnes in total in 2023.

China’s domestic resources are limited relative to that scale, and the geopolitics of uranium supply, concentrated in Kazakhstan, Canada, and Australia, are not straightforwardly friendly to a country whose relationships with Western suppliers have been under sustained pressure. Theoretically at that fleet size, the spent fuel from China’s PWRs could theoretically keep 70 to 75 AFCRs running with no additional natural uranium input, taking a meaningful bite out of both the waste management problem and the uranium import dependency simultaneously.

The AFCR does require reprocessing infrastructure: the recovered uranium must first be chemically separated from fission products through PUREX or equivalent processing before it can be blended with depleted uranium tails. However, China is already building two reprocessing plants at 200 tonnes per year each, so that piece of the puzzle is in motion regardless.

The cost of NUE fuel is higher than fresh natural uranium and fabrication challenges remain, which is a genuine limitation, but China has consistently demonstrated that it is willing to pay a premium for reactor technologies that extend its strategic capabilities like the HTR-PM high-temperature gas-cooled reactor at Shidao Bay and CFR-600 sodium fast reactor at Xiapu.

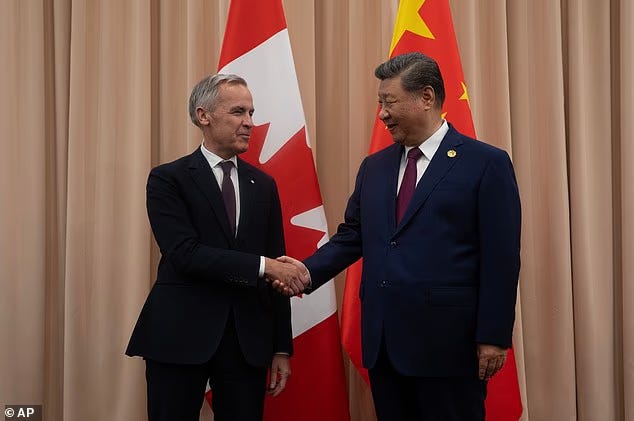

The AFCR sits in a similar space: it does not minimize near-term electricity cost, but it partially closes China’s fuel cycle using a commercially proven reactor platform. Prime Minister Carney’s recent state visit to China included AtkinsRéalis in the delegation. The AFCR conversations, St. Julian said, are restarting.

Reviving the 1980’s Golden Age of CANDU

The domestic supply chain question is where the gap between ambition and execution is most concrete. Today approximately 100,000 workers are sustained by the Canadian nuclear industry, primarily by the Bruce and Darlington and now Pickering refurbishment programs. The refurbishments have been running for about fifteen years, which means the supply chain has had a longer warm-up period than most observers credit. St. Julian describes this as a significant advantage over competitors: “Canada is well ahead of, I call it, the power curve.” The Americans attempting to ramp up an AP1000 supply chain essentially from a standing start, and the French working to reconstitute capacity for EPR2, are trying to do something that Canada has been doing continuously, if at reduced scale, for a decade and a half.

The most important gap St. Julian identified in the CANDU supply chain is heavy water supply. Existing Canadian inventory can cover the first one or two new units by drawing on surplus from Pickering and Gentilly, but a twelve-reactor build-out in Ontario would require production capacity that does not currently exist in Canada. AtkinsRéalis has signed a memorandum of understanding with Argentina, whose state nuclear technology company designed heavy water plant, Planta Industrial de Agua Pesada (PIAP) at Arroyito has been in operation for roughly forty years and was taken offline about seven years ago; AtkinsRéalis is helping restart it, intends to take off-take from it, and sees the process design as licensable for a Canadian facility. Bruce Power, Ontario Power Generation (OPG), and AECL are all participating in the working group addressing this.

The recent thaw in Canada-India relations opens a further pathway. Prime Minister Carney’s March 2026 visit to New Delhi produced a landmark $2.6 billion agreement for Saskatoon-based Cameco to supply nearly 22 million pounds of uranium to India for its civilian nuclear program, alongside a new Strategic Energy Partnership and explicit commitments to cooperate on reactor technology.

India operates the world’s largest heavy water production complex and has decades of experience with CANDU-derived reactors. There is a satisfying narrative symmetry in the emerging relationship: Saskatchewan uranium fueling Indian reactors, Indian heavy water filling Canadian CANDUs.

Team CANDU?

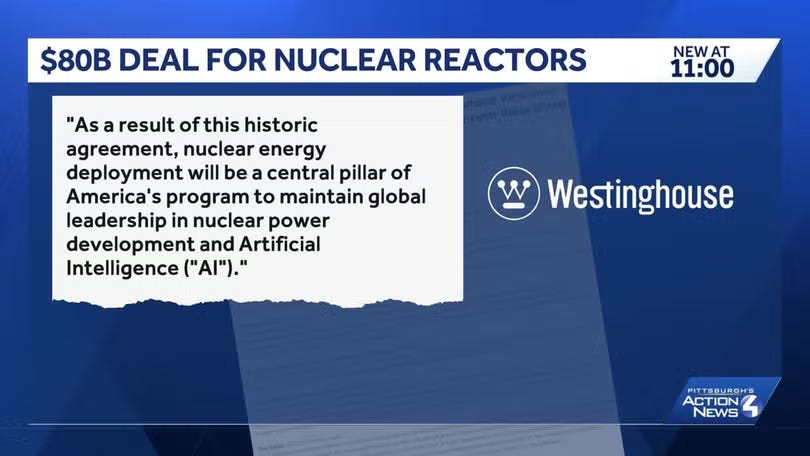

St. Julian was direct about where the heavier political economy question sits. The US federal government has committed to support the AP1000 program through an $80 billion investment in Westinghouse and committing to assist with financing, streamline permitting, and facilitate construction. In exchange, the government receives a profit participation of 20 percent of any cash distributions above $17.5 billion, and holds the option to require a Westinghouse IPO by 2029 and convert that interest into a 20 percent equity stake. Separately, the DOE has designated four federal reservations: Oak Ridge, Savannah River, Paducah, and Idaho National Laboratory, sites originally acquired through eminent domain for the weapons program, as co-location zones pairing nuclear power generation with hyperscaler data centers as anchor load customers

The U.S. government is not simply financing the program; it is taking a position in the upside. Despite this federal commitment, Westinghouse has no active supply chain and limited construction capacity for the program it has just been handed.

Canada’s situation is structurally the opposite with an active supply chain and workforce. What Canada lacks is the political architecture that converts that industrial inheritance into a coordinated program.

St. Julian said AtkinsRéalis is in early discussions with both the federal government and provincial governments about whether something structurally analogous to the US model makes sense for CANDU, not an American-style program, he was careful to say, but some form of direct investment that would allow the Crown to benefit not just from GDP and tax receipts but from a greater return on the technology it originally funded.

Canada already participates in the upside from CANDU deployment, but it does so through an upstream mechanism tied to intellectual property rather than through direct project ownership or visible revenue sharing at the plant level.

When the federal government sold the CANDU reactor division of Atomic Energy of Canada Limited to SNC-Lavalin in 2011, it retained ownership of the core CANDU intellectual property. The commercial entity, now operating as Candu Energy under AtkinsRéalis, was granted a long term license to deploy and monetize that technology globally. In return, AECL receives royalties tied to new builds, refurbishments, and related engineering services. These payments are structured as royalties tied to future reactor sales, life extensions, and certain products and services, with the government projecting potential recovery in 2011 of up to $285 million over roughly 15 years though the precise payment formula has not been publicly disclosed.

The practical effect is that Canada captures value from every CANDU project, but indirectly. The government does not take an equity stake in individual plants, does not receive a per megawatt hour production royalty, and does not participate explicitly in project level cash flows. The return is embedded in licensing revenue, supplemented by domestic supply chain activity and tax receipts. The actual royalty receipts have never been publicly disclosed.

The contrast with the U.S. government Westinghouse deal is therefore structural. Canada operates as an intellectual property landlord, collecting a slice of revenue through licensing while leaving project economics to private developers and utilities. The emerging U.S. model places the state closer to the asset itself, aligning public returns more directly with reactor deployment and performance.

Getting the Band Back Together

In 1982 there were approximately 100,000 people working simultaneously in the CANDU supply chain, thirteen reactors under construction domestically and internationally at a single point in time, federal and provincial governments aligned with Crown utilities like Ontario Hydro, AECL as the technical authority, and a constellation of engineering firms and manufacturers operating in coordinated roles in a Team Canada approach.

That synergy has subsequently fractured over thirty-five years of privatization, restructuring, and new-build drought. AtkinsRéalis is now one of several large engineering firms, alongside Kinectrics, WSP, Stantec, and Hatch, where once AECL and Ontario Hydro were the organizing center. The construction contractors, Aecon, Bird, PCL, are capable but were not built around a continuous CANDU new-build program. The supply chain of 250 manufacturers exists, has been spooling up through the refurbishments, and in St. Julian’s phrase, is “fully capable” if not yet at the capacity a fleet build requires.

“We are in the early stages of getting the band back together,” he said. That being said the Team Canada framing is coherent only if Canada actually decides to field a team and play ball.

Picking that team, and backing it with the kind of structural commitment the US has made to AP1000, would mean converting a latent industrial advantage into an actual program. The raw materials for that program are more intact than the twenty-year new-build gap suggests. The refurbishments are the crawl: fifteen years of continuous work that kept the supply chain active, drove the cost curve down unit over unit, and gave the CNSC enough confidence in the refurbished Darlington design to license it for another twenty years. The Cernavodă contract is the walk: the first partial new CANDU construction since 2007, generating real cost and schedule data where before there were only projections. The domestic fleet build, twelve reactors in Ontario if the program goes the distance, is the run. Canada is approaching the transition from refurbishment to sustained new-build.

When new CANDUs break ground, the workforce stepping onto those sites will not be starting from scratch. The tools remain in place, and the institutional memory has been sustained through decades of refurbishment and ongoing engineering work. The supply chain now sees a credible pipeline of projects for the first time since the 1980s, which changes the nature of the challenge. Reassembling large scale build capacity becomes a problem of coordination and scaling, rather than reconstruction. Whether Canada chooses to mobilize these capabilities toward sustained deployment is the billion dollar question.

This essay accompanies Decouple’s conversation with Joe St. Julian, president of nuclear at AtkinsRéalis. Watch on YouTube, or listen on Apple and Spotify. If you find our work valuable, consider supporting Decouple by pledging on Substack or making a tax-deductible donation through our fiscal sponsor at Givebutter.

The longer an article, the harder it is to maintain coherence, and this was done beautifully. While I would like to see V.C. Summer 2 and 3 completed, and four more reactors built in Texas, I full agree with the logic of the strength of the Canadian nuclear technology and the timing-is-everything current net positive public support. Go forth, be fruitful and multiply.

A great article, well written and an uplifting story about Canadian ingenuity. My concern on implementation would be the ties between Brookfield, Westinghouse and the current PM. Will he back the opportunity to create a world beating nuclear architecture made in Canada over Westinghouse partially owned by Brookfield where he was the chairman? There is also the Canadian Cameco partnership in Westinghouse that presents political challenges. We will see but I am cheering for Candu because we can do here when we choose to.